THE MISSING LINK IN FINANCIAL PLANNING

June 17, 2026The Missing Link in Financial Planning Part 7

July 1, 2026

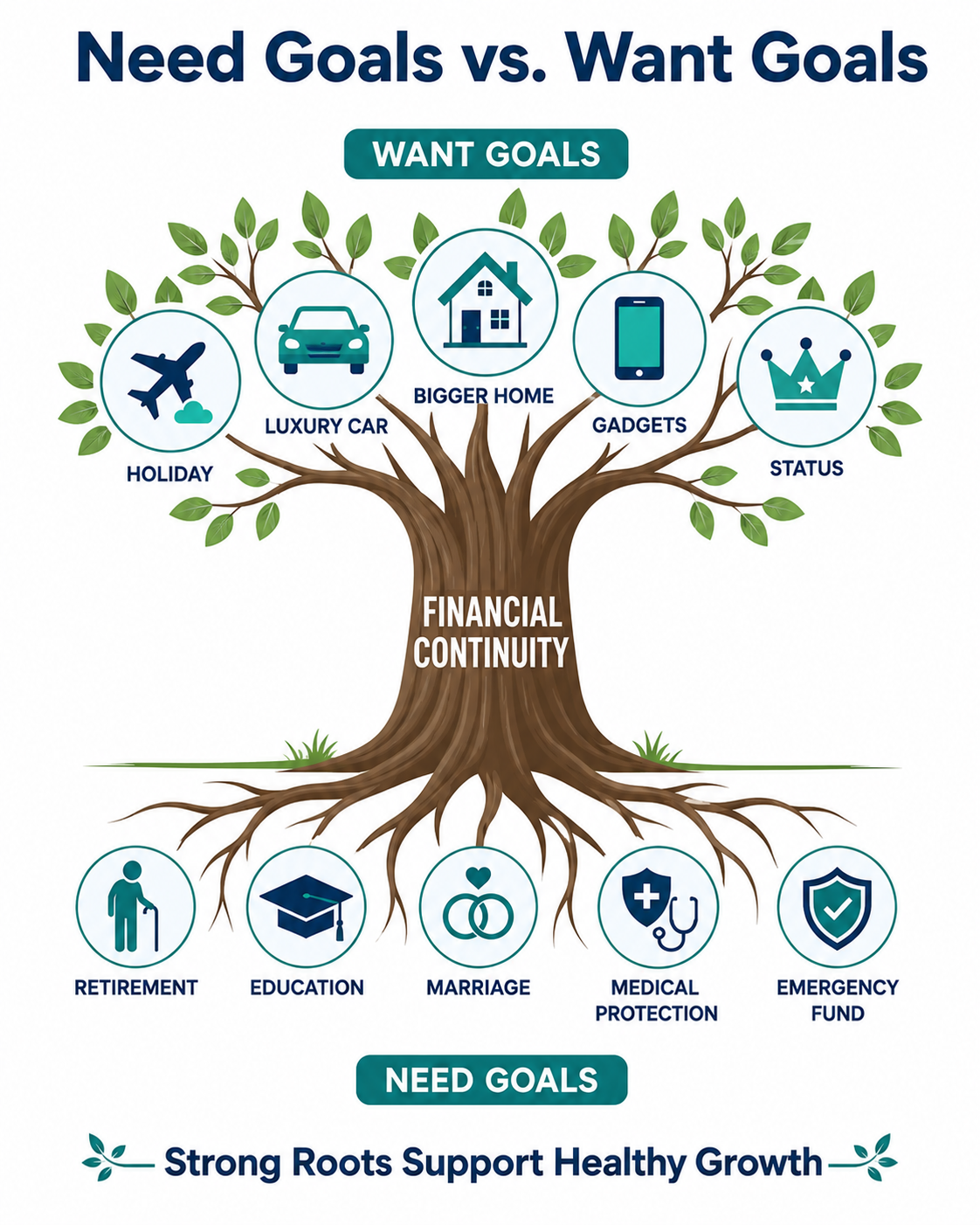

Need Goals vs Want Goals

In the earlier parts of this series, I explored why many financial plans fail despite good products and good returns, and how investor behaviour often impacts long-term financial outcomes more than investment performance itself.

In Part 1, I introduced the role of discipline and continuity in making long-term compounding work.

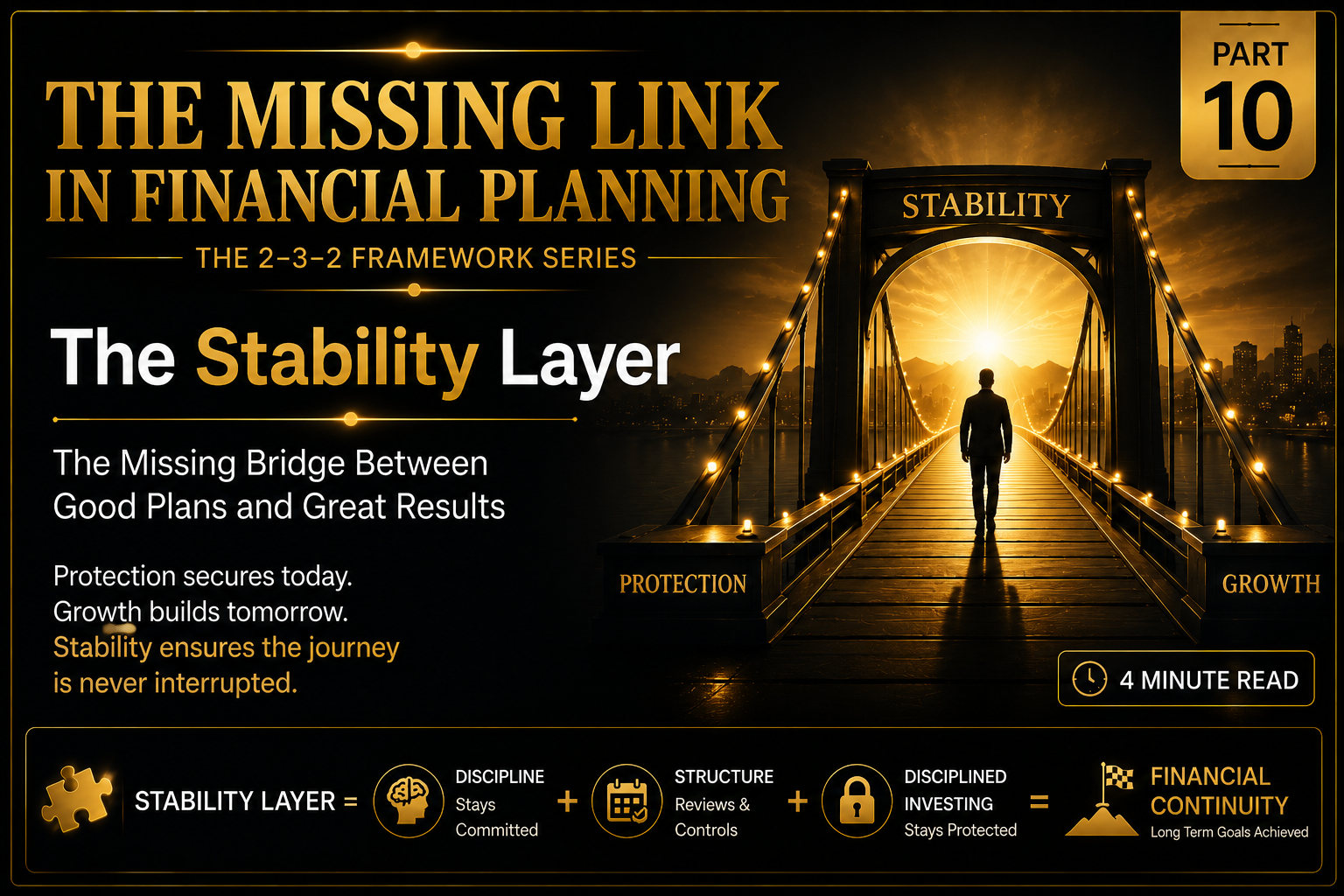

In Part 2, I explored the Stability Layer as a missing dimension in traditional financial planning.

In Part 3, I explained the difference between Investment Volatility Risk and Behavioural Discipline Risk.

In Part 4, I introduced the 2–3–2 Framework consisting of 2 Gaps, 3 Layers, and 2 Risks.

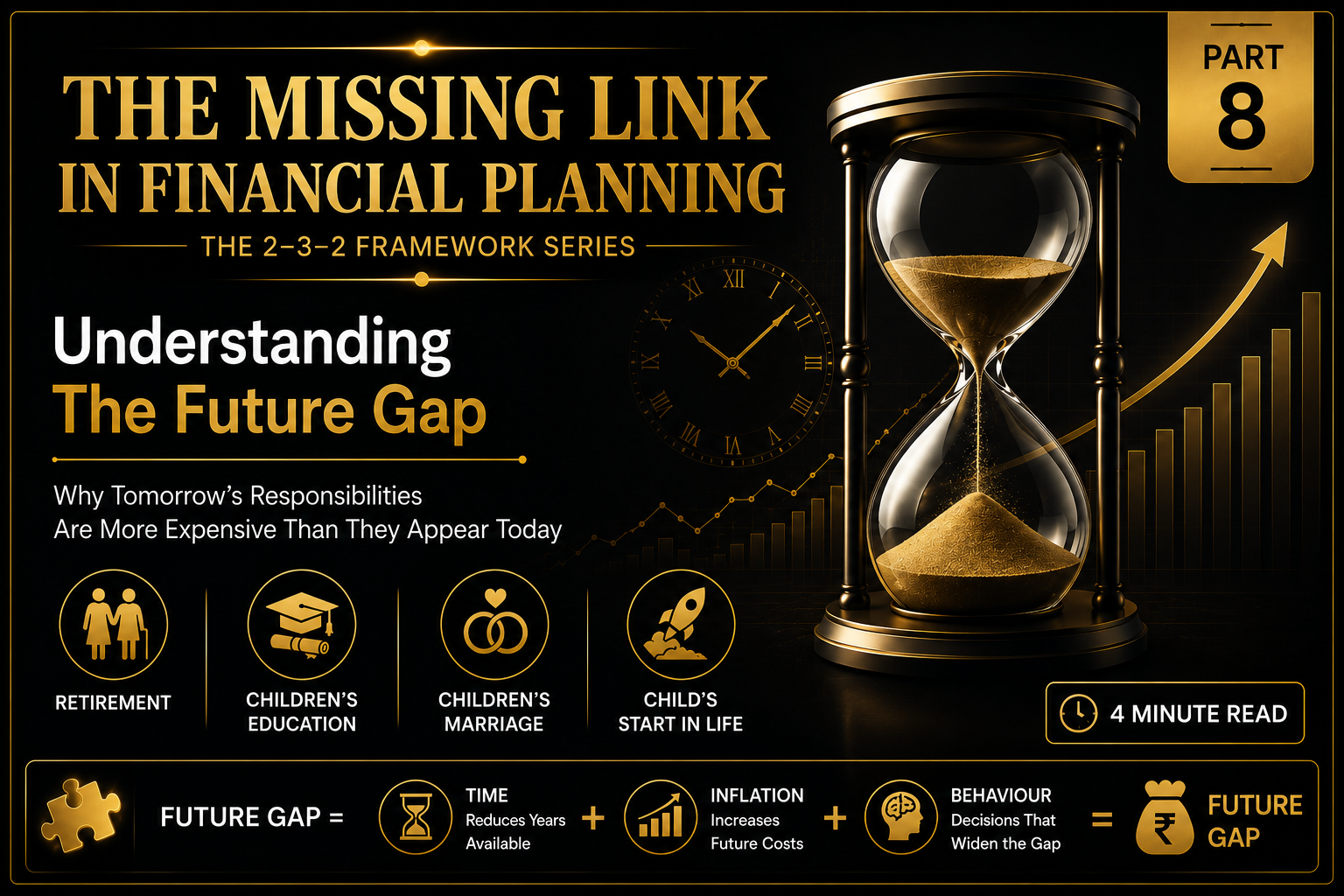

In Part 5, I introduced the two financial gaps every family must fund — the Present Gap and the Future Gap.

But knowing the gaps is not enough.

The real challenge lies in how families allocate their money.

This is where the great conflict begins.

Every family constantly faces a choice between:

Need Goals

and

Want Goals

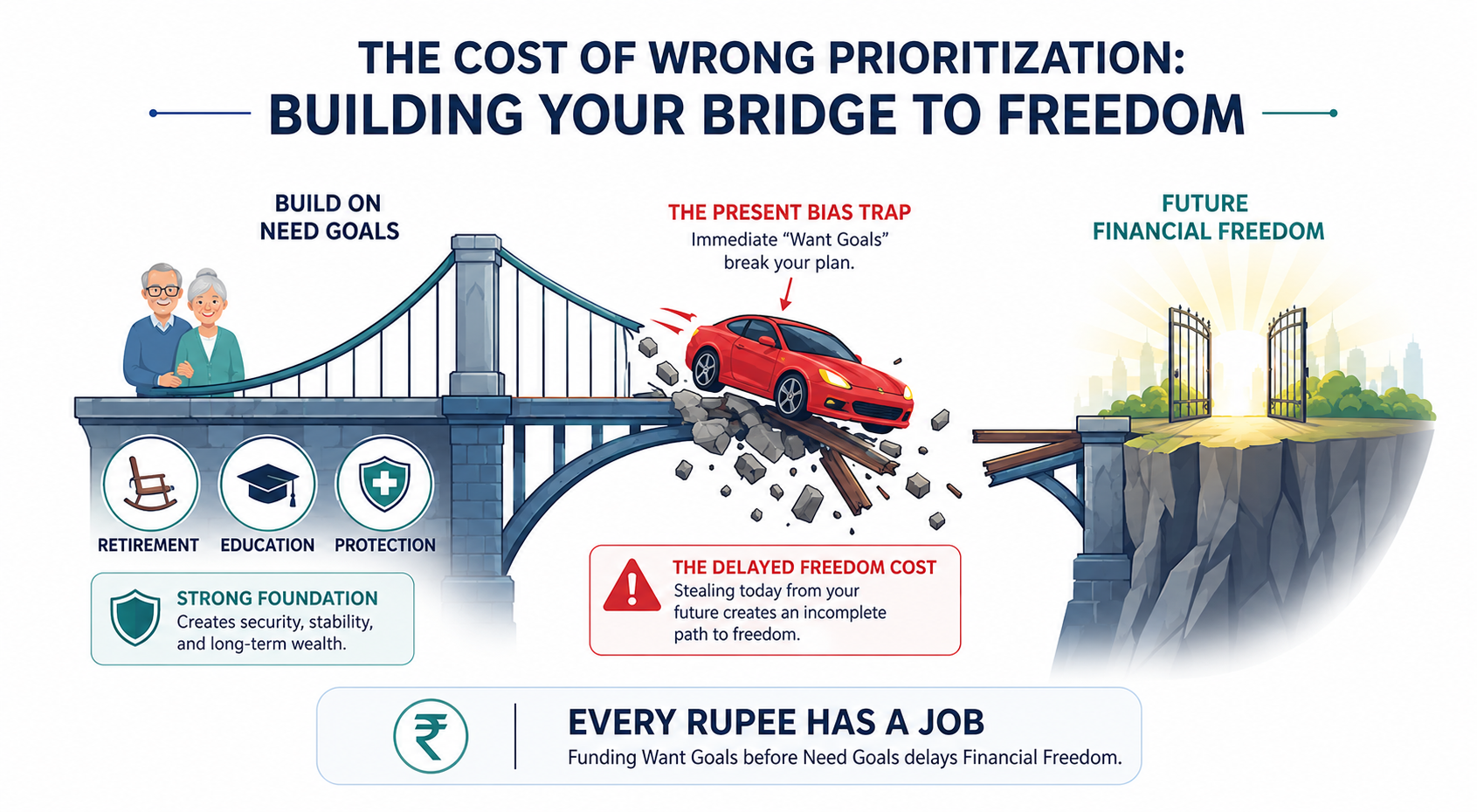

Need Goals

Need Goals are those that directly affect a family’s dignity, continuity, and long-term financial security.

These include:

- Retirement

- Children’s education

- Children’s marriage

- Medical protection

- Income replacement

- Emergency reserves

If these goals are not funded adequately, families may eventually be forced to compromise their lifestyle and financial independence.

Need Goals are rarely exciting because their benefits are often distant and invisible. Yet they are the foundation of long-term financial continuity.

Want Goals

Want Goals are desirable but not essential.

These include:

- Foreign holidays

- Luxury car upgrades

- Bigger homes than required

- Lifestyle upgrades

- Expensive gadgets

- Status purchases

There is absolutely nothing wrong with Want Goals.

The problem begins when Want Goals are funded before Need Goals.

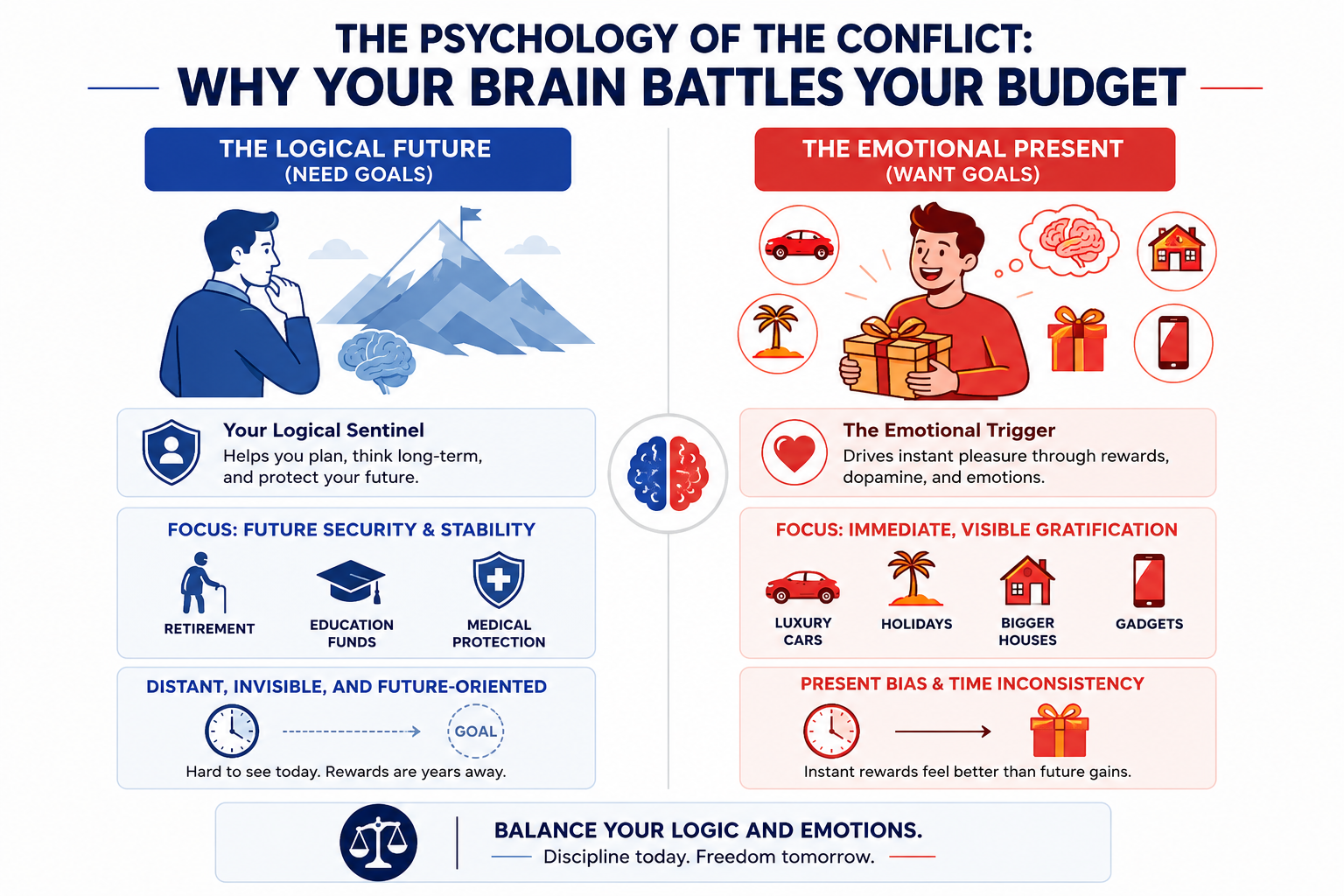

The Psychology Behind It

Need Goals are:

- Future-oriented

- Distant

- Emotionally invisible

Want Goals are:

- Immediate

- Visible

- Emotionally rewarding

As a result, the human mind naturally gravitates toward Want Goals.

Future pain is invisible.

Present pleasure is visible.

This simple psychological reality is responsible for many financial failures.

Having worked with more than 2,000 families over four decades, I have repeatedly seen Want Goals quietly displace Need Goals.

A Real-Life Example

One of my clients, Mr. Dwivedi , was a middle-level manager in a pharmaceutical company.

We had created a financial plan focused on funding his children’s education, which was still 15 to 17 years away then.

Five years later, he called and requested that I withdraw the investments earmarked for that goal.

The reason?

He had found what he believed was the perfect house at an attractive price and felt it was an opportunity he could not afford to miss.

I explained the difference between Need Goals and Want Goals and the consequences of disrupting a long-term plan.

However, the emotional attraction of owning that house was stronger than the distant benefit of funding his children’s education.

The investments were withdrawn.

A year later, when we reviewed his finances, he discovered that the new EMI commitments had significantly reduced his ability to continue investing for his children’s future.

The plan never fully recovered.

Several years later, when higher education expenses arrived, he had no choice but to take an education loan at a stage in life when carrying additional debt became financially stressful.

The house brought immediate satisfaction.

The education loan brought delayed consequences.

The Cost of Wrong Prioritization

The tragedy is not that people fail financially because they earn too little.

Many fail because they consistently prioritize what is visible, enjoyable, and immediate over what is important.

Lifestyle upgrades often happen gradually.

A bigger house.

A better car.

A more expensive vacation.

Individually, these decisions may appear harmless.

Collectively, they can quietly weaken the funding of critical Need Goals.

In my first article, I referred to the famous Marshmallow Experiment, where only a small percentage of children resisted immediate gratification for a larger reward later.

Financial planning presents the same challenge throughout adult life.

The ability to delay gratification often determines long-term financial success.

Connection to the Stability Layer

The Stability Layer exists precisely to protect Need Goals from being repeatedly sacrificed at the altar of Want Goals.

Its purpose is not to eliminate aspirations or lifestyle improvements.

Its purpose is to ensure that long-term financial security is not compromised by short-term temptations.

Financial freedom is not achieved simply because income increases.

It is achieved when families consistently fund their Need Goals before pursuing their Want Goals.

Income creates opportunity.

Discipline creates financial continuity.

In my next article, I will explore the Present Gap in greater detail — its purpose, its consequences, and why it is one of the most overlooked dimensions of financial planning.

If you have not read the Previous Blogs then Link for Blog 1