The Missing Link in Financial Planning – Part 4

June 10, 2026

The Missing Link in Financial Planning Part 6

June 24, 2026

Part 5

The Two Financial Gaps Every Family Must Fund

In the earlier parts of this series, I explored why many financial plans fail despite good products and good returns, and how investor behaviour often impacts long-term financial outcomes more than investment performance itself.

In Part 1, I introduced the idea that discipline and continuity play a critical role in making long-term compounding work.

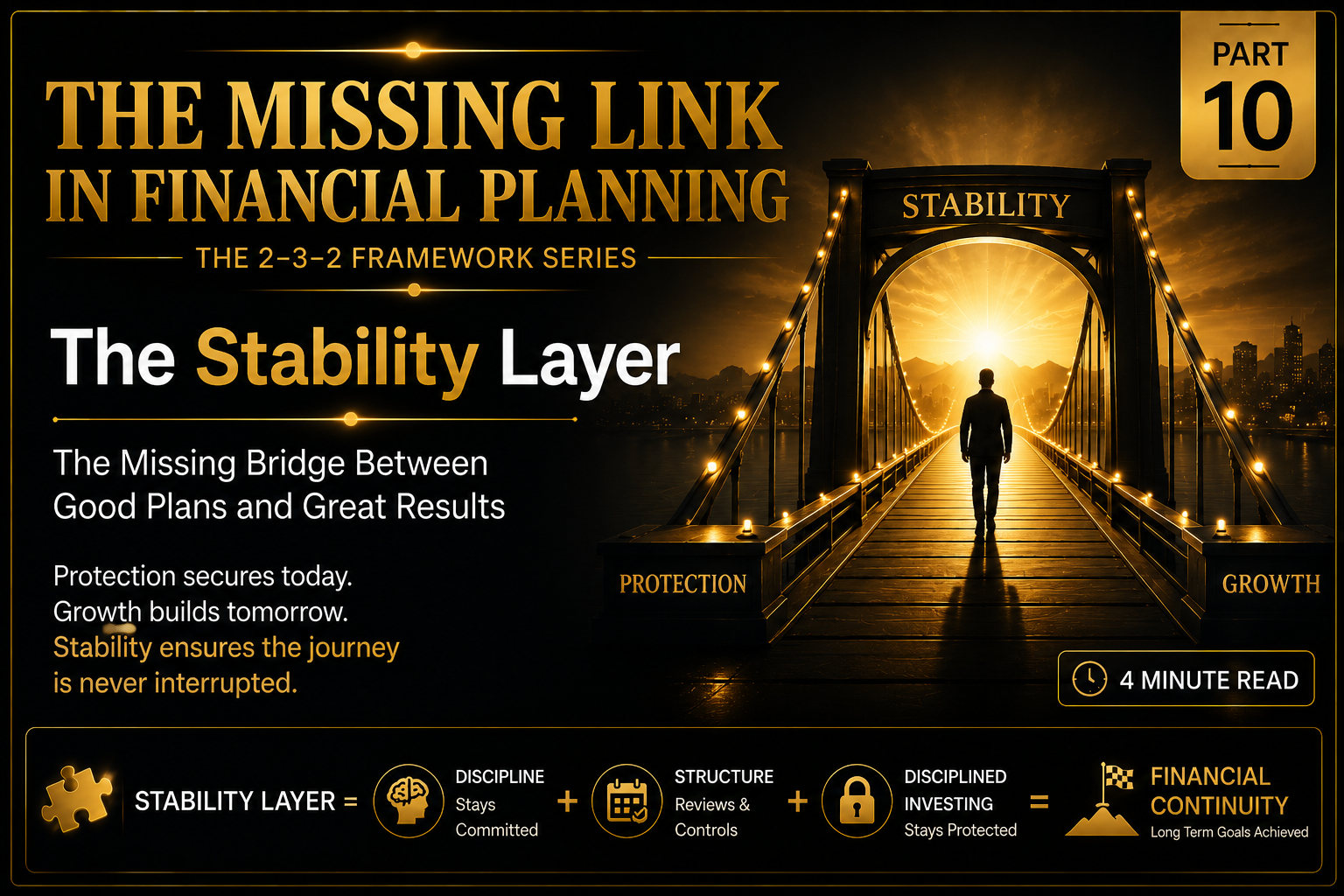

In Part 2, I explored the concept of the Stability Layer as a missing dimension in traditional financial planning.

In Part 3, I explained the difference between Investment Volatility Risk and Behavioural Discipline Risk, and why both affect long-term outcomes differently.

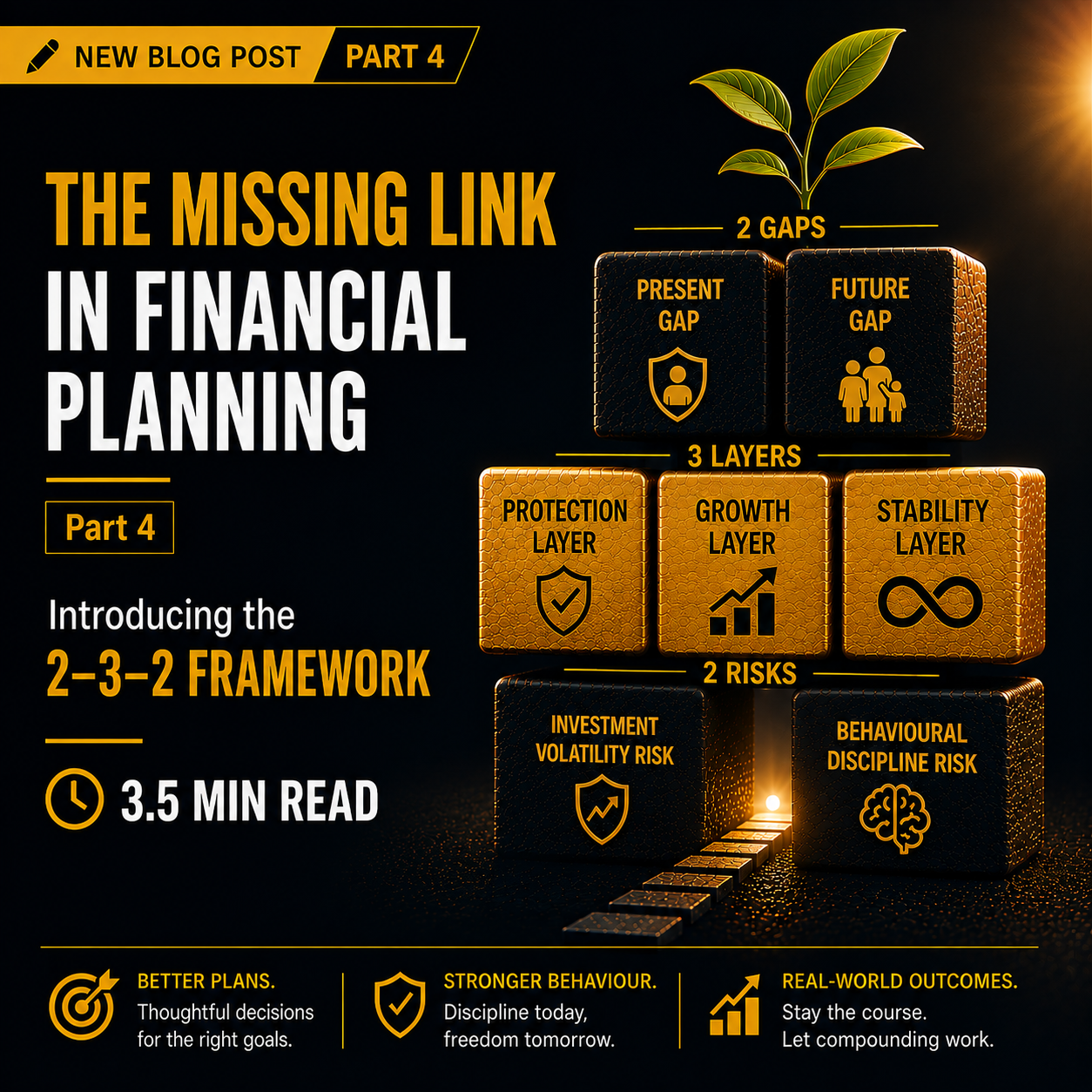

In Part 4, I introduced the 2–3–2 Framework consisting of:

2 Gaps, 3 Layers, and 2 Risks.

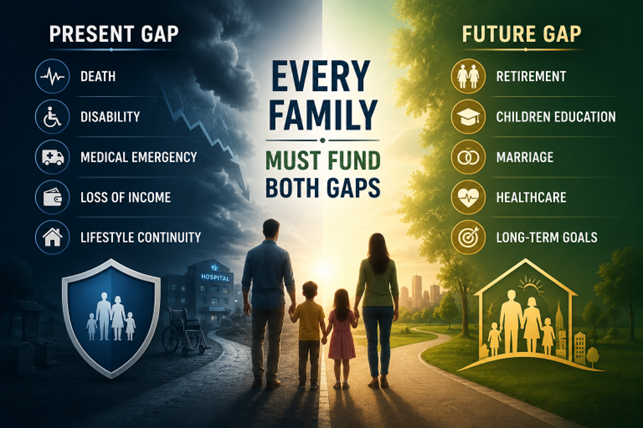

One of the most important parts of this framework is understanding the two financial gaps every family must fund — the Present Gap and the Future Gap.

Many families feel financially safe today because they have recurring income and are comfortably maintaining their lifestyle.

As long as income continues flowing and expenses are managed smoothly, life appears financially stable.

But this sense of comfort can often be misleading.

Over the years, I observed that families unconsciously move through four broad stages of financial life — Creation of Income, Consumption of Income, Continuation of Income, and finally Conservation of Income.

The most neglected stage is often the Continuation of Income, where families create financial continuity by funding both the Present Gap and the Future Gap.

The Present Gap

The Present Gap refers to the financial deficiency that may arise today because of:

- death

- disability

- temporary income loss

- medical emergencies

- loan obligations

- lifestyle continuity needs

In simple words, the Present Gap asks:

“If income stops today, can the family continue maintaining its current lifestyle?”

One of my clients, Mr. Raju (name changed), was a senior executive in a highly successful company. He enjoyed an excellent lifestyle supported heavily by company-provided accommodation, car, driver, medical benefits, and other executive privileges.

Because life was comfortable and income was strong, the family naturally assumed that everything was financially secure.

However, during our discussions, I repeatedly tried to explain that much of the lifestyle was dependent on company perquisites rather than personal financial continuity planning.

Unfortunately, Mr. Raju passed away unexpectedly at a relatively young age.

Almost overnight, the family had to vacate the company bungalow, lose the official car and other facilities, and drastically reduce their lifestyle. The insurance cover was inadequate, and there was insufficient liquid corpus available to maintain continuity.

The emotional trauma of the loss was severe enough. But the sudden collapse of financial continuity made the situation even more painful for the family.

This experience deeply reinforced my belief that many families mistake current income and lifestyle for long-term financial security.

In reality, they may simply have an unfunded Present Gap.

Many families also underestimate the enormous corpus actually required to maintain continuity.

For example, if a family requires ₹10 lakh annually to maintain its lifestyle, the corpus required to generate that income sustainably may exceed ₹3 crore.

Most families are shocked when they realize the size of this gap.

The existing liquid investments, savings, and insurance protection available to the family determine how much of this Present Gap is already funded and how much still remains uncovered.

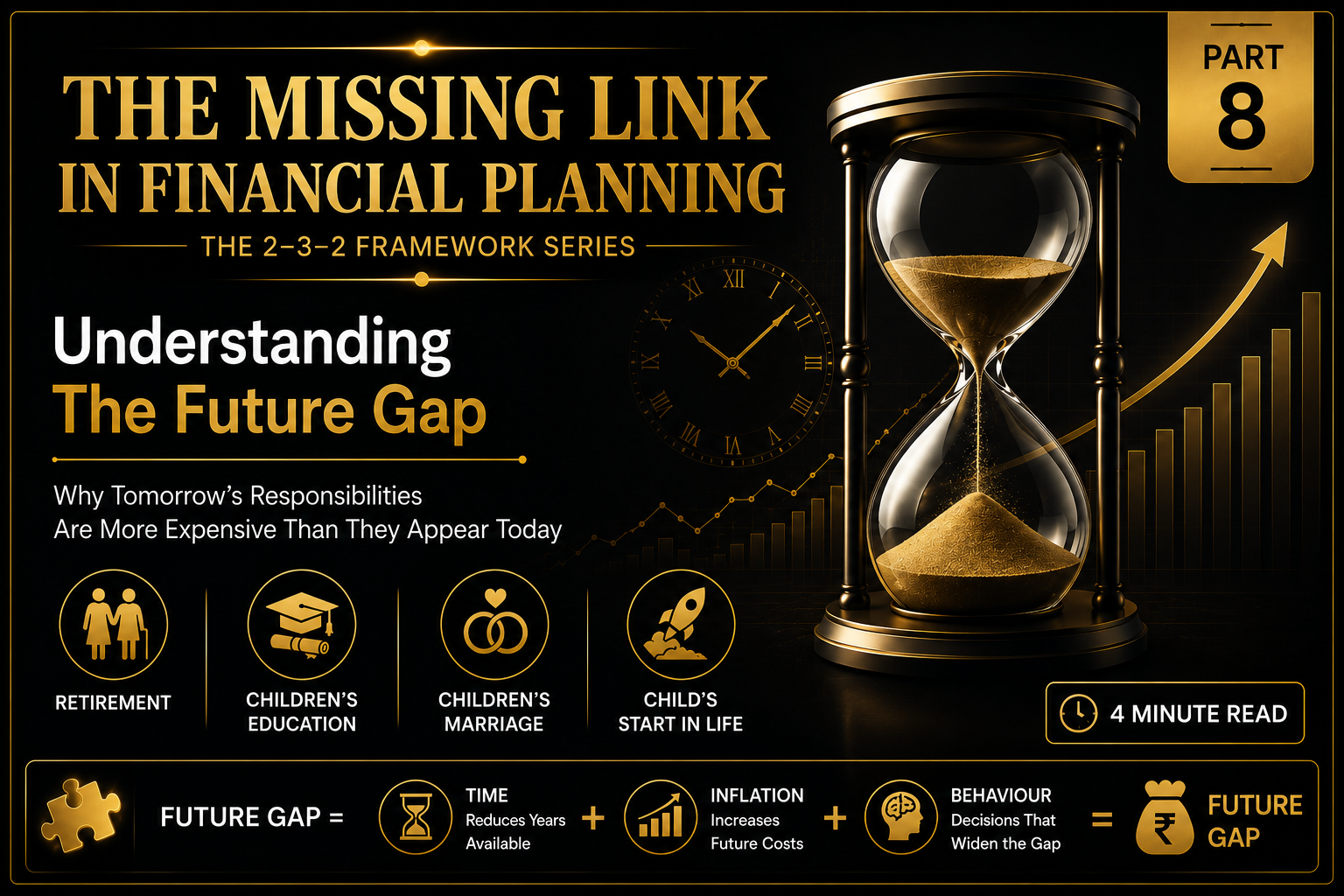

The Future Gap

The Future Gap refers to the capital required for future responsibilities such as:

- retirement

- children’s education

- marriage planning

- healthcare needs

- other long-term Need Goals

Unlike the Present Gap, these responsibilities appear distant and therefore emotionally less urgent.

This is where many investors become behaviourally vulnerable.

Immediate gratification often dominates long-term planning. Lifestyle upgrades, vacations, luxury spending, and Want Goals quietly begin replacing the discipline required to fund future Need Goals.

Inflation further enlarges these future gaps silently over time.

A retirement goal that appears manageable today may become financially overwhelming two decades later if continuity and compounding are interrupted.

This is why identifying and calculating both the Present Gap and the Future Gap is critical.

Without understanding these gaps clearly, financial planning often remains generic instead of becoming truly personalized and meaningful.

Perhaps the real objective of financial planning is not merely wealth creation.

It is the creation of long-term financial continuity for the family. In my next article, I will explore one of the biggest behavioural conflicts in financial planning — Need Goals versus Want Goals — and why many investors unknowingly sacrifice long-term financial security for short-term gratification

If you have not read previous Blogs

Link to 1st Blog Part 1 :