The Missing Link in Financial Planning – Part 3

June 3, 2026

THE MISSING LINK IN FINANCIAL PLANNING

June 17, 2026

Introducing the 2–3–2 Framework

In my earlier three articles, I explored why many financial plans fail despite good products and good returns, introduced the Stability Layer as a missing dimension in financial planning, and explained the difference between Investment Volatility Risk and Behavioural Discipline Risk.

As I reflected on four decades of working with more than 2,000 families, I gradually realized that long-term financial continuity depends on understanding:

• the financial gaps families must fund

• the layers required to support those goals

• and the behavioural risks that interrupt continuity along the way

This realization eventually led me towards what I now call the:

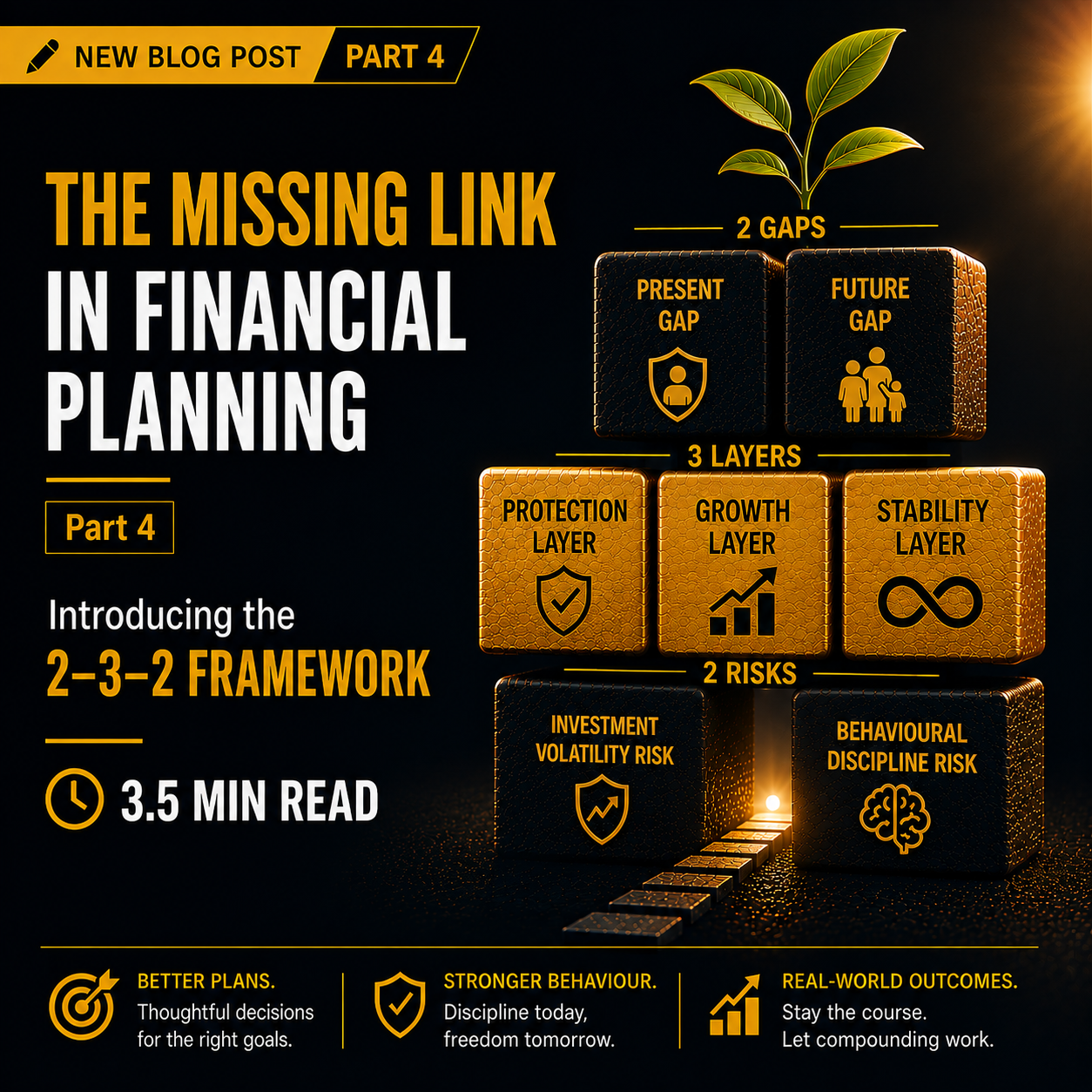

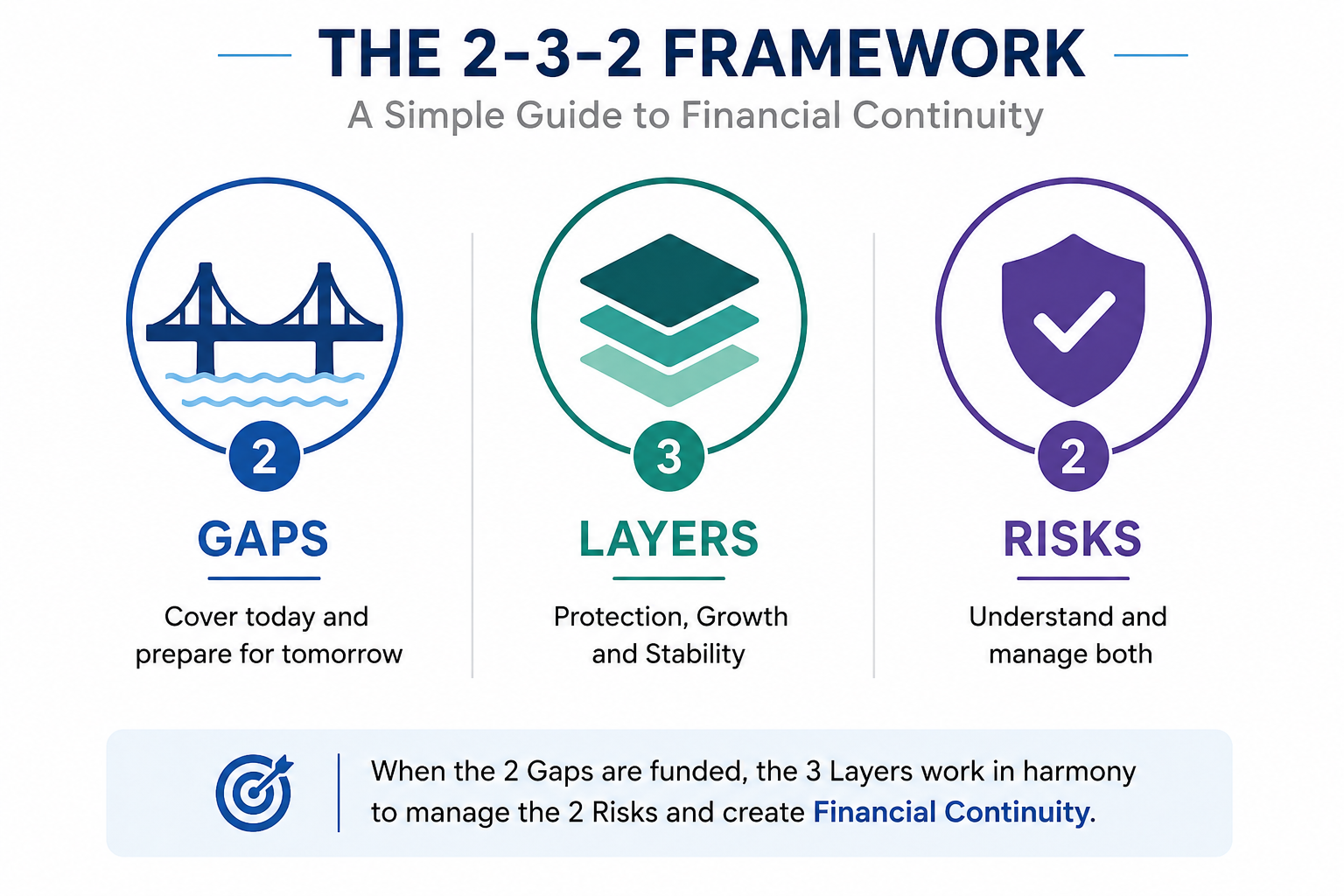

2–3–2 Framework

2 Gaps

3 Layers

2 Risks

Over the years, I became increasingly uncomfortable with traditional financial planning. I observed that many people with proper asset allocation, good returns, and sincere intentions still failed to achieve their long-term financial goals.

The issue was not always the products.

The issue was often the absence of a structure that accommodated human behaviour and emotional decision-making.

Most financial plans are designed logically. But people often deal with money emotionally.

Clients frequently fail to differentiate between Need Goals and Want Goals. Immediate gratification often overrides long-term commitments, creating behavioural risks that are rarely addressed structurally within traditional financial planning.

I deliberately kept the framework simple because financial planning should not feel academic or complicated. Investors should be able to easily understand the risks, remember the structure, and appreciate the consequences of deviating from long-term discipline.

The 2 Gaps

The first part of the framework focuses on the two financial gaps every family must fund.

Present Gap

The Present Gap refers to the financial protection required today in the event of:

• unfortunate death

• disability

• temporary loss of income

• medical emergencies

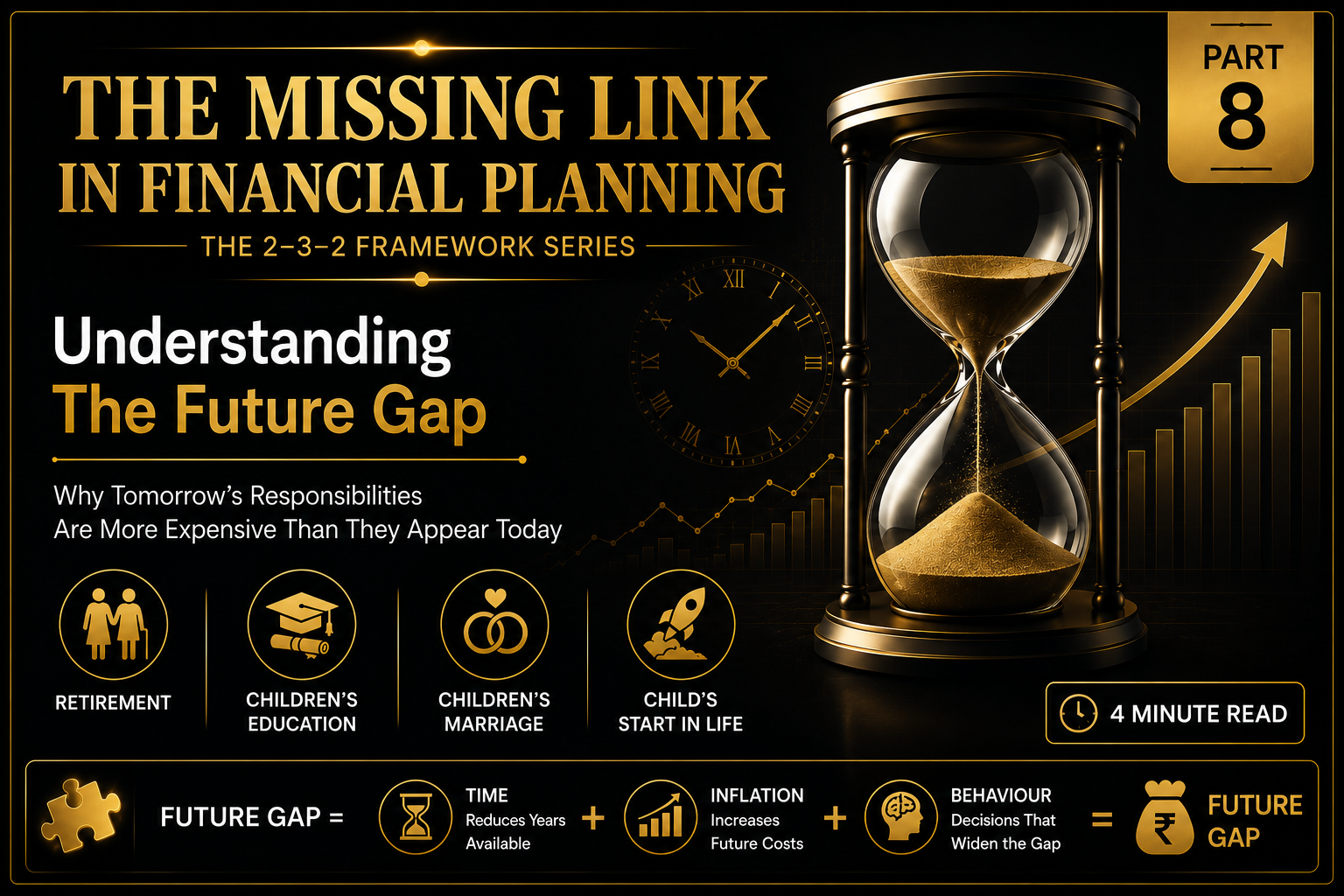

Future Gap

The Future Gap refers to future responsibilities such as:

• children’s education

• children’s marriage

• retirement funding

These are primarily Need Goals that directly affect the long-term stability and dignity of the family.

One of my clients, Mr. Raju was a senior executive in a mid-sized company. He enjoyed a luxurious lifestyle supported heavily by company-provided accommodation, car, and other benefits.

During our discussions, I repeatedly explained the importance of evaluating his lifestyle independently of these company perquisites and planning for a future financial reality.

Unfortunately, he passed away unexpectedly at a young age.

The family had to vacate the company bungalow, lose all company benefits, and drastically alter their lifestyle almost overnight. The insurance cover was inadequate, and the family was financially unprepared for the transition.

This experience reinforced to me how important it is to correctly identify and fund both the Present Gap and the Future Gap before a crisis exposes the financial weakness of the family structure.

The 3 Layers

The second part of the framework focuses on the three layers required to support long-term financial continuity.

Protection Layer

The Protection Layer helps families manage the Present Gap through insurance and emergency protection structures.

Growth Layer

The Growth Layer helps create long-term wealth to fund future responsibilities and goals.

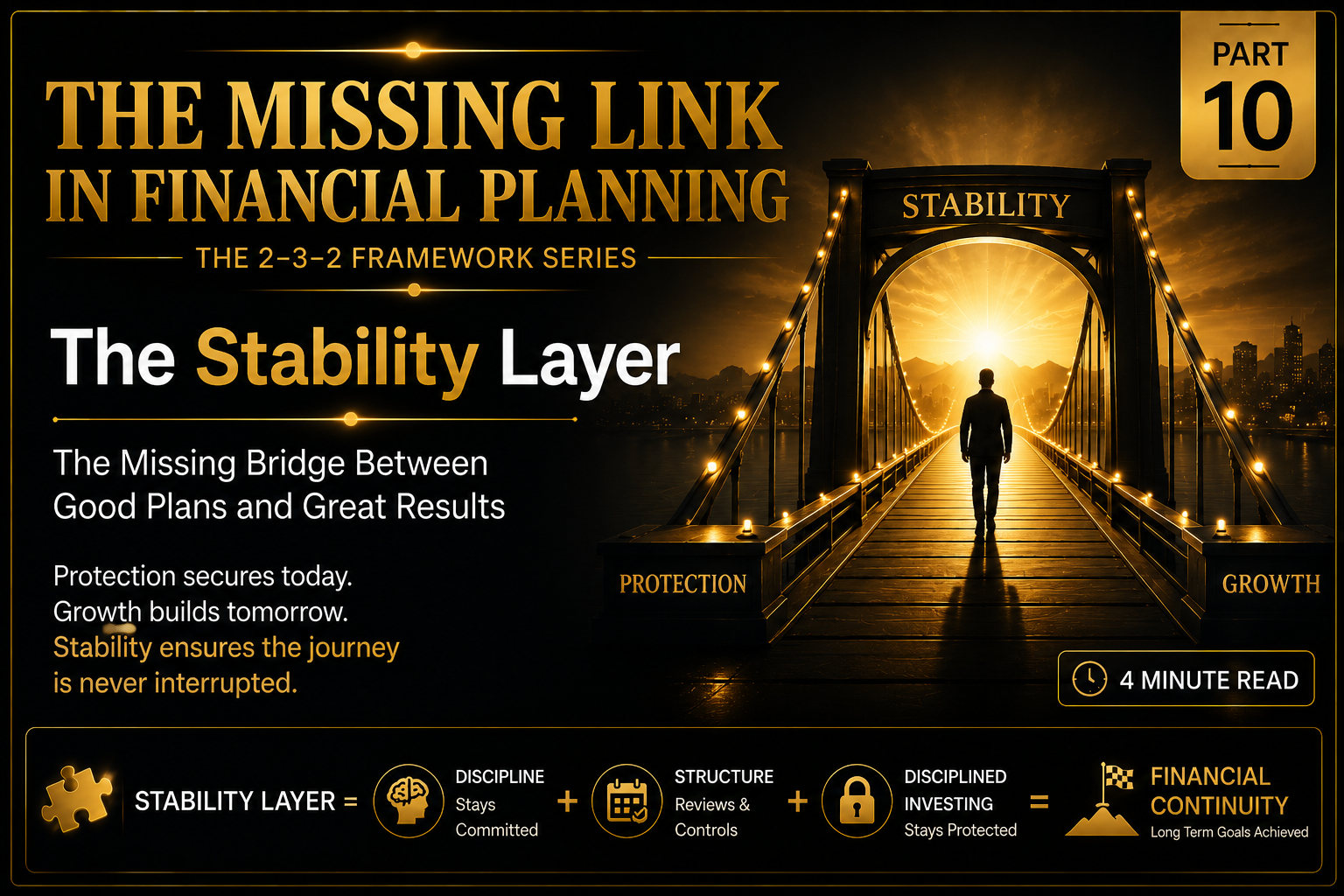

Stability Layer

The Stability Layer is designed to help investors remain committed to the financial journey long enough for compounding to work effectively.

Traditional financial planning already addresses Protection and Growth reasonably well.

However, through years of observation, I realized that many investors still failed because continuity itself was breaking midway through the journey. Investments were started enthusiastically but interrupted repeatedly because of emotional decisions, lifestyle temptations, or shifting priorities.

This is where the Stability Layer becomes critical.

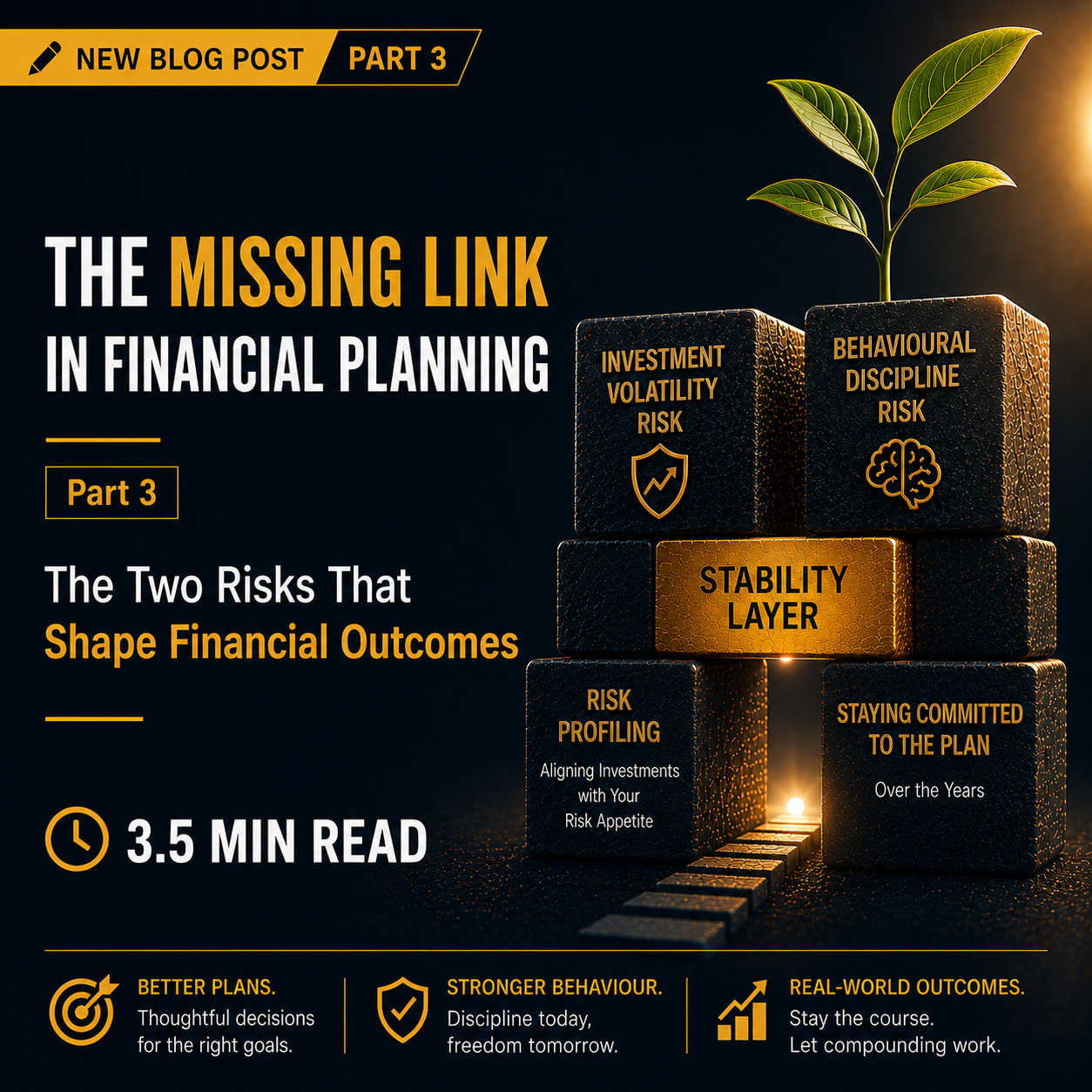

The 2 Risks

The third part of the framework focuses on the two risks that affect long-term financial outcomes.

Investment Volatility Risk

This is the fear investors experience during market corrections and volatility. Traditional risk profiling handles this risk effectively through proper asset allocation.

Behavioural Discipline Risk

This is the risk of long-term financial continuity breaking because of emotional decisions, impulsive spending, or Want Goals overriding Need Goals.

In my experience, this second risk is often underestimated despite its significant impact on long-term outcomes.

Why This Framework Matters

Long-term financial success is not determined only by selecting the right products or earning high returns.

It also depends on remaining committed to the journey long enough for compounding to work.

Many investors fail not because investments performed poorly, but because continuity itself broke along the way.

Perhaps the future of financial planning will not depend only on better products and better returns, but also on creating structures that help investors remain behaviourally consistent over decades.

In my next article, I will explore the two financial gaps every family must fund — the Present Gap and the Future Gap.

Previous blogs- The Missing Link in Financial Planning Part 1 :

Link to NEXT Blog PART 5 :