The Missing Link in Financial Planning – Part 2

May 27, 2026

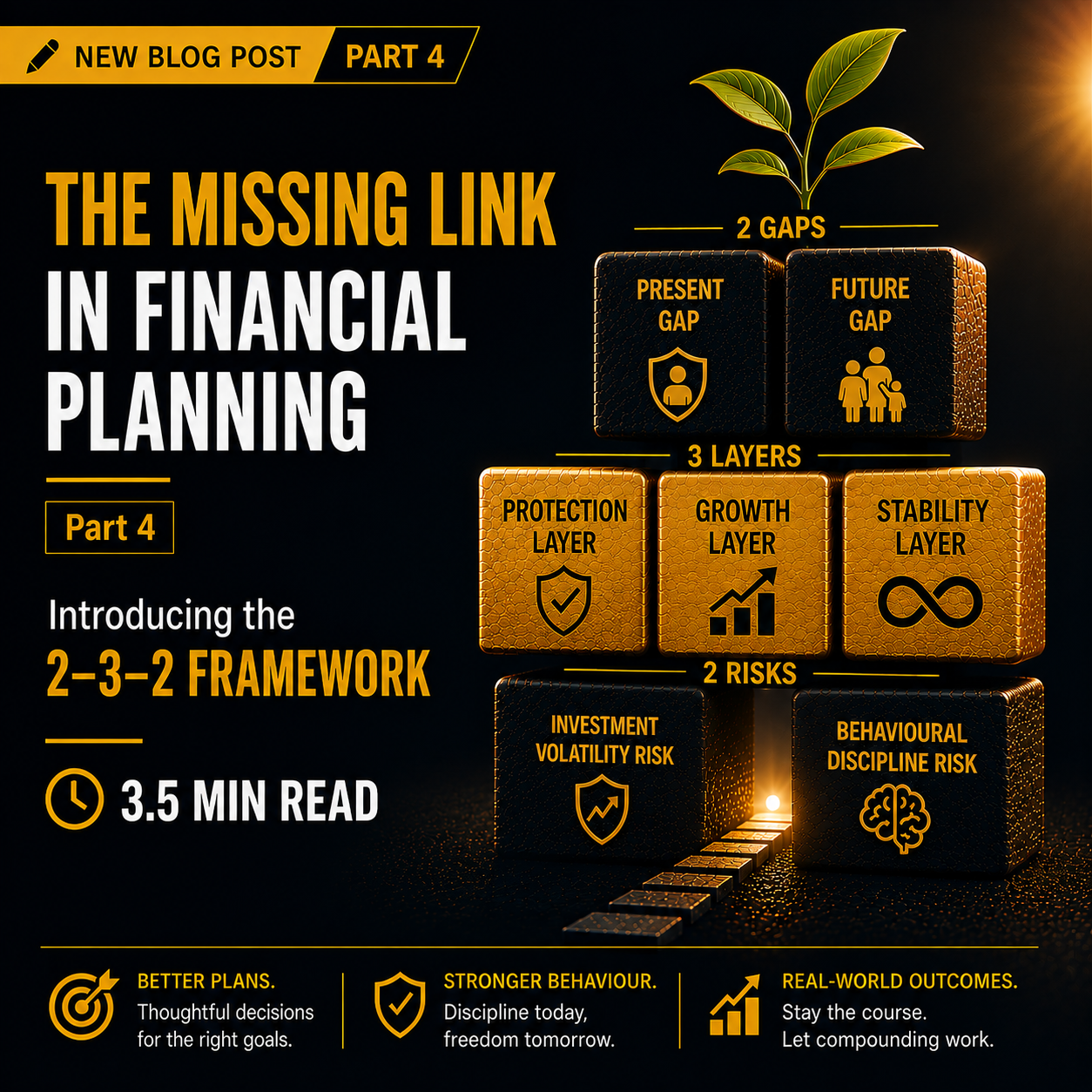

The Missing Link in Financial Planning – Part 4

June 10, 2026

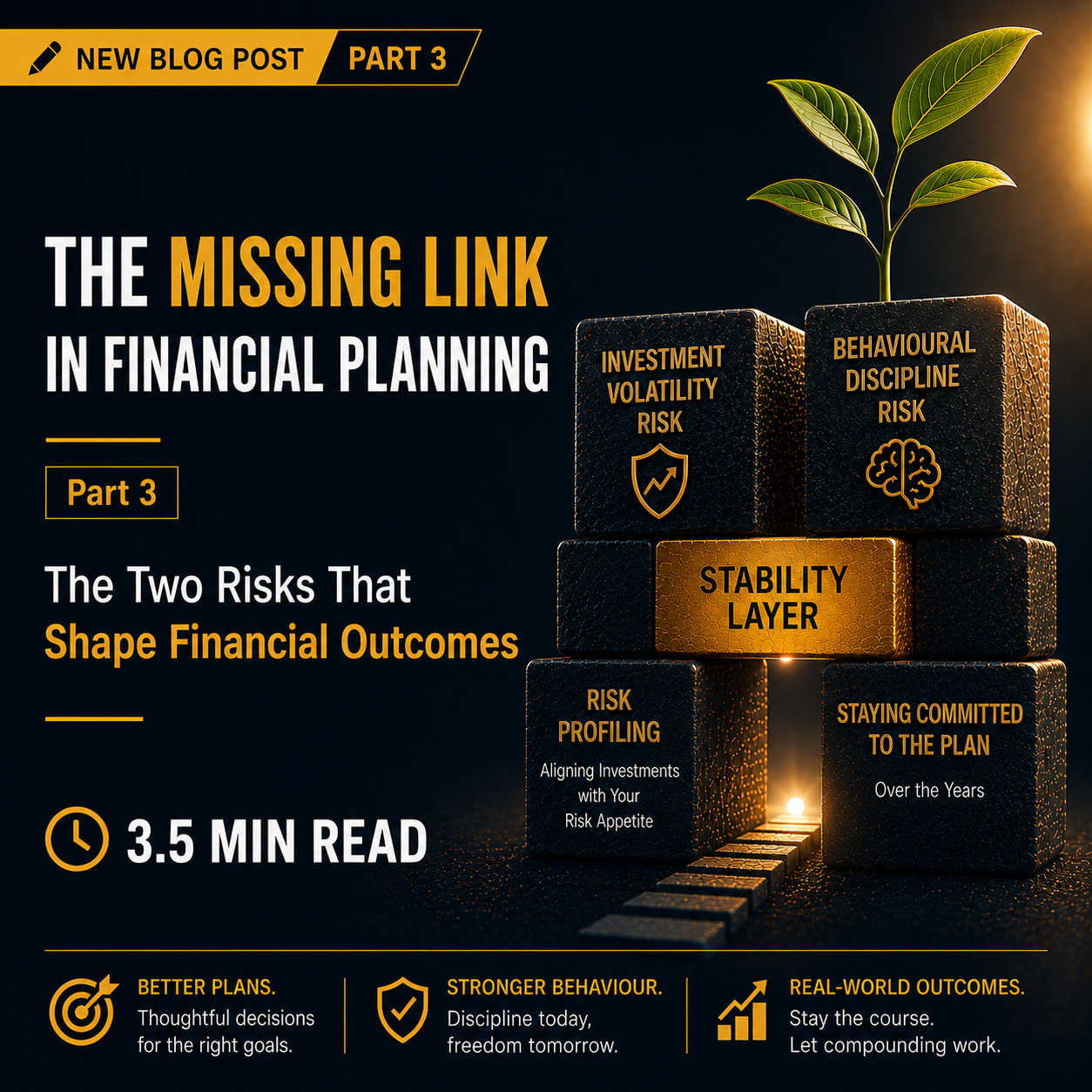

The Two Risks That Shape Financial Outcomes

In my first article, I introduced the idea that discipline often matters more than returns in achieving long-term financial outcomes. In the second article, I introduced what I call the Stability Layer — a missing dimension that helps investors remain committed to their financial journey.

As I reflected further on my experiences working with more than 2,000 families over four decades, I realized that there are actually two very different risks that shape financial outcomes.

Most investors and even many advisors tend to treat them as one and the same.

They are not.

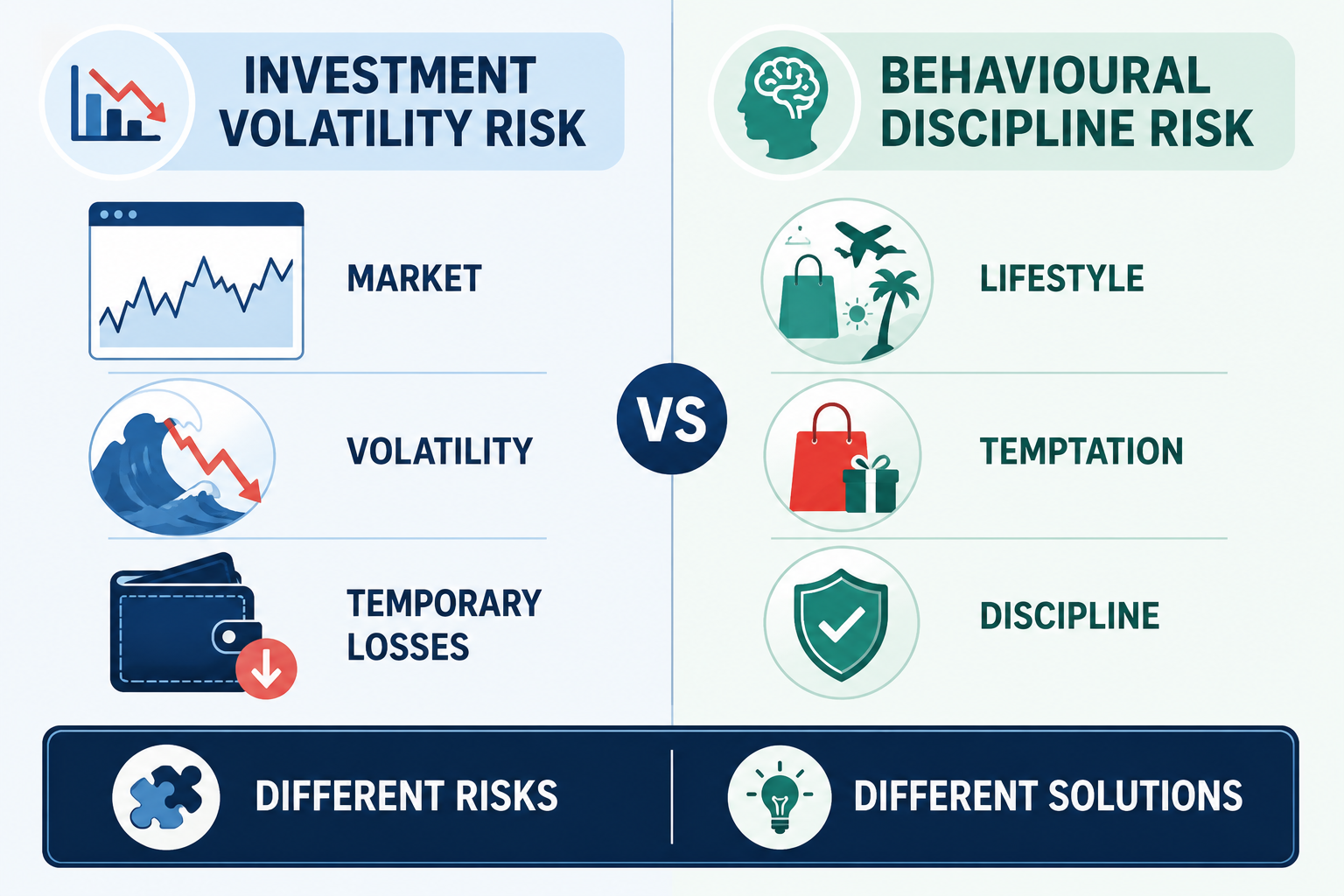

The two risks are:

- Investment Volatility Risk

- Behavioural Discipline Risk

Investment Volatility Risk

Investment Volatility Risk refers to an investor’s ability to handle market fluctuations and temporary losses.

Traditional financial planning addresses this risk through Risk Profiling.

Investors are typically categorized as Aggressive, Moderate, or Conservative based on their reactions to market volatility and uncertainty.

The objective is simple: align the asset allocation with the investor’s temperament so that he or she does not panic during market downturns.

Over the years, I have seen this process work remarkably well.

For example, one of my clients, Mr. Anand (name changed), was around 60 years old with a secure pension and very little dependence on his investments for day-to-day living. Despite his age, his risk profile showed him to be highly aggressive. Market corrections hardly bothered him.

On the other hand, another client, Mr. Deepak (name changed), was only 40 years old but had experienced significant losses during the Harshad Mehta era. His profile showed him to be conservative despite his younger age.

These examples taught me an important lesson.

Age alone does not determine risk appetite. Risk profiling often captures the emotional reality of the investor far better than assumptions based on age.

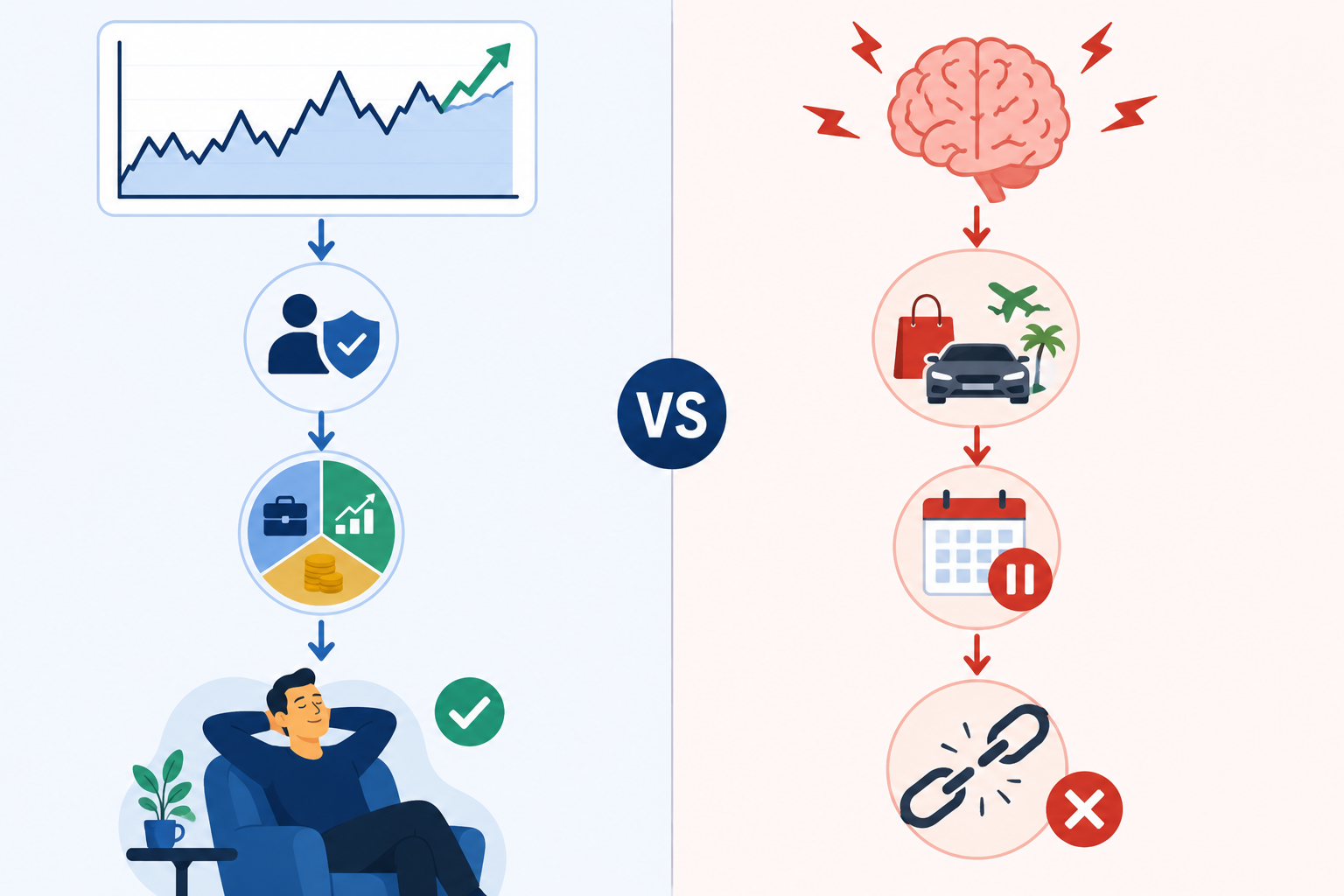

In my experience, traditional financial planning handles Investment Volatility Risk extremely well.

Behavioural Discipline Risk

However, there is another risk that is very different.

I call it Behavioural Discipline Risk.

This is not about how investors react to falling markets.

It is about their ability to stay committed to a financial plan over long periods of time.

Many financial plans assume that once a plan is created, investors will naturally follow it for years or even decades.

My experience suggests otherwise.

Most investors are not purely logical beings trying to maximize returns. They are emotional human beings trying to balance aspirations, temptations, fears, desires, and social pressures.

Over the years, I have seen investors interrupt long-term plans because of:

• Lifestyle upgrades

• Impulsive spending

• Real estate diversions

• Liquidity temptations

• Delayed restarting after interruptions

• Loss of focus on long-term goals

This risk exists even when:

• The portfolio is well designed

• Returns are satisfactory

• The advisor is competent

In other words, the plan is not failing because of the market.

The plan is failing because continuity is breaking.

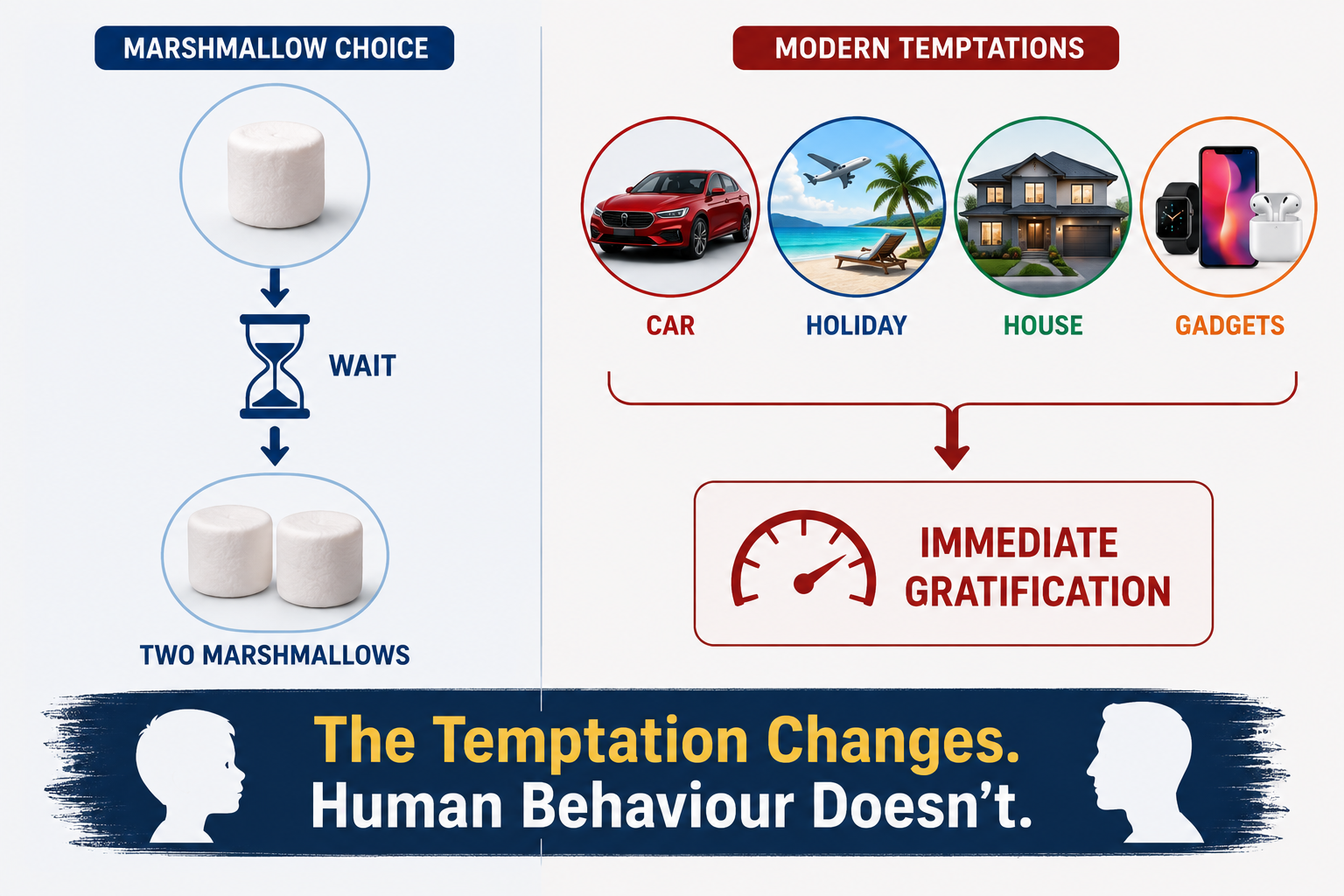

One of the most fascinating examples of this behaviour comes from the famous Stanford Marshmallow Experiment.

Children were given a simple choice: eat one marshmallow immediately or wait and receive two marshmallows later.

A majority found it difficult to delay gratification.

As I reflected on decades of investor behaviour, I realized that adults are often no different.

The temptation simply changes form.

The marshmallow becomes a new car, a luxury holiday, a property purchase, a lifestyle upgrade, or some other immediate desire.

Many investors who are perfectly capable of handling market volatility still struggle with behavioural discipline.

I noticed that several aggressive investors were not failing because they feared market corrections.

They were failing because continuity itself was breaking.

This led me to a simple distinction:

Investment Risk = Ability to tolerate market volatility

Behavioural Discipline Risk = Ability to sustain financial continuity over long periods

Industry data supports this reality. Reports from Cafe Mutual suggest that only a small percentage of investors remain invested long enough to fully benefit from compounding. Choosing the right investment is important, but staying invested may be even more important.

Both risks affect outcomes.

But they require completely different solutions.

Traditional financial planning already does an excellent job of managing Investment Volatility Risk.

The bigger challenge is Behavioural Discipline Risk — the ability to stay committed to a plan long enough for compounding to work its magic.

Perhaps the future of financial planning will not depend only on selecting better products, but also on designing structures that help investors remain behaviourally consistent over decades.

In my next article, I will introduce the 2–3–2 Framework and explain how the Stability Layer is designed to address Behavioural Discipline Risk and improve the probability of long-term financial success.

If you have not read previous Blogs Link to Blog PART 1 : https://laazarusdias.in/2026/05/19/why-financial-planning-fails-despite-good-returns/

Link To Next Blog PART 4 :