When Victory Becomes Dangerous

May 6, 2026

The Missing Link in Financial Planning – Part 2

May 27, 2026Why Financial Planning Fails Despite Good Returns Part 1

What is the goal of financial planning?

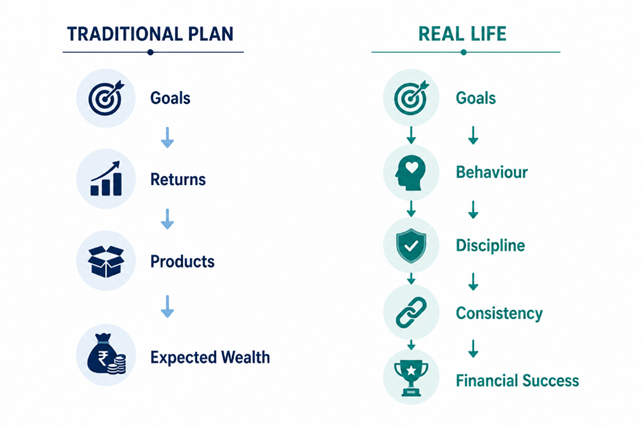

At its core, financial planning seeks to identify a client’s goals, assign present and future values to those goals based on inflation, and design an investment strategy to fund them over time. The plan typically relies on systematic investments across instruments, with a strong focus on expected portfolio returns.

So far, everything seems logical and well-structured.

However, there is one critical assumption that is rarely documented, discussed, or even acknowledged:

That the investor will remain disciplined—consistently investing year after year, regardless of market ups and downs.

From my experience of 4 decades dealing with 2000 families , I have learnt that most financial plans are built on sound return assumptions, diversified portfolios, and long-term projections. Yet, in real life, many investors still struggle to achieve the intended outcomes.

Why does this happen?

The common explanation is market volatility. But in practice, the real reason is different.

Financial planning focuses on returns—but long-term success depends on behaviour and structure.

Traditional financial planning works for disciplined investors—but for most, outcomes are driven by behaviour in the absence of structure.

The Behavioural Reality

The truth is simple:

- People are emotional, not purely logical

- Decisions are influenced by fear, temptation, and liquidity

- Discipline often weakens during uncertainty

Consider two individuals.

Mr. A is highly disciplined. He commits to investing ₹10,000 every month for 25 years and follows through without interruption. In fact, he simply preserves the money consistently without chasing returns.

Mr. B, on the other hand, is financially aware and selects an investment capable of delivering 18% annual returns. However, he lacks discipline. He stops investing intermittently and withdraws funds during market fluctuations.

Who is more likely to build wealth over time?

In most real-world scenarios, Mr. A outperforms Mr. B—not because of superior returns, but because of consistent behaviour.

Consistency is the first level of wealth creation.

Returns come next.

The Missing Dimension: Discipline Profiling

In financial planning, we routinely perform risk profiling to determine whether an investor is aggressive or conservative.

But we rarely assess something equally important:

Discipline.

Discipline is not an abstract concept—it is measurable.

An investor’s past behaviour, saving patterns, and response to volatility provide clear indicators.

Without incorporating discipline into planning, there is a disconnect between projected outcomes and real-world results.

This creates a significant disconnect between projected outcomes and real-world behaviour.

A large proportion of investors—often the majority—are unable to stay invested long enough for compounding to work effectively. As a result, financial goals are compromised—not due to poor products, but due to behavioural deviations.

A Structured Approach: Beyond Returns

Financial planning needs to evolve from being return-centric to being structure-driven.

A more complete approach can be viewed through three elements:

1. Two Gaps

- Present Gap: The immediate capital required to protect the family in case of loss of income

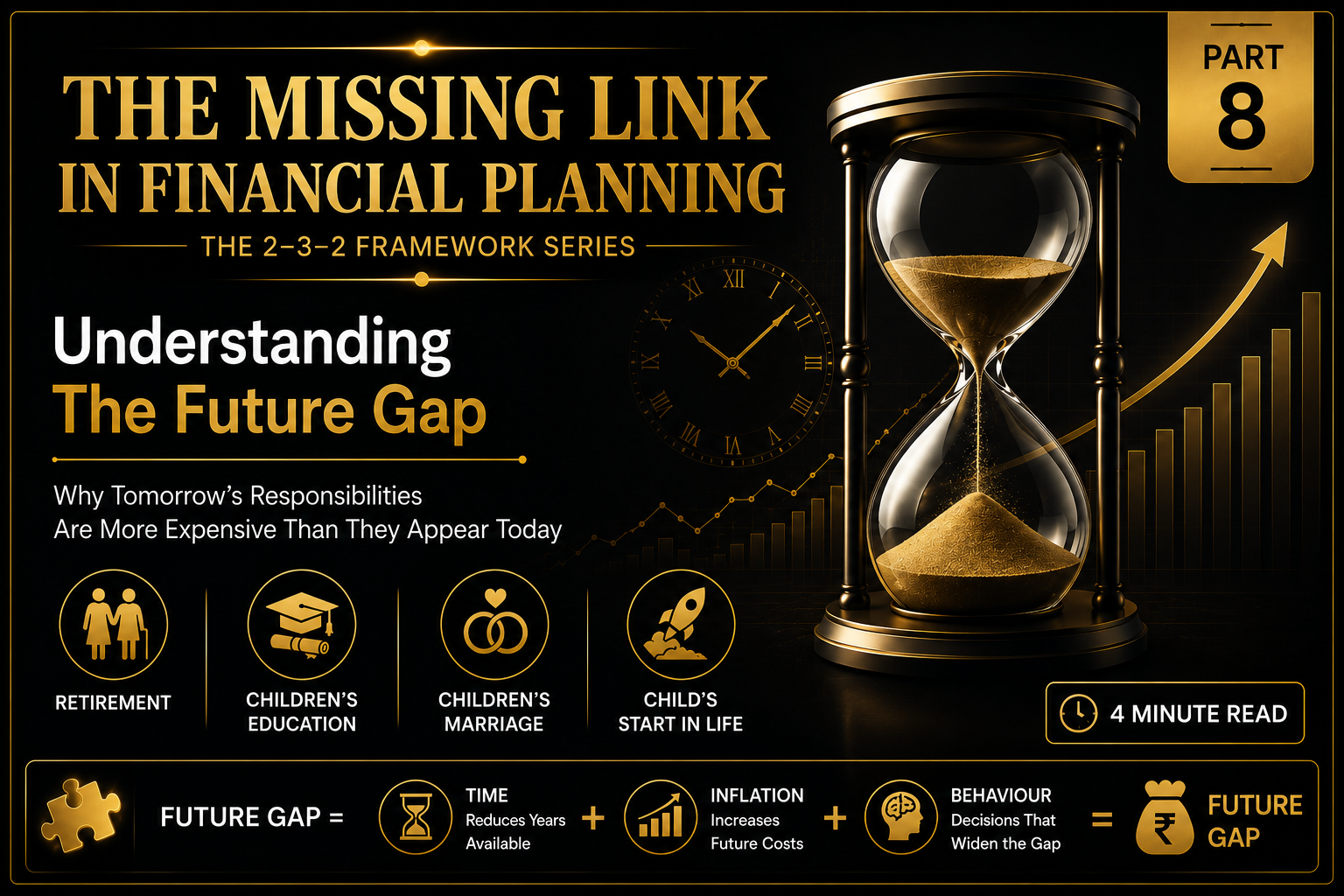

- Future Gap: The corpus required to sustain long-term goals such as retirement

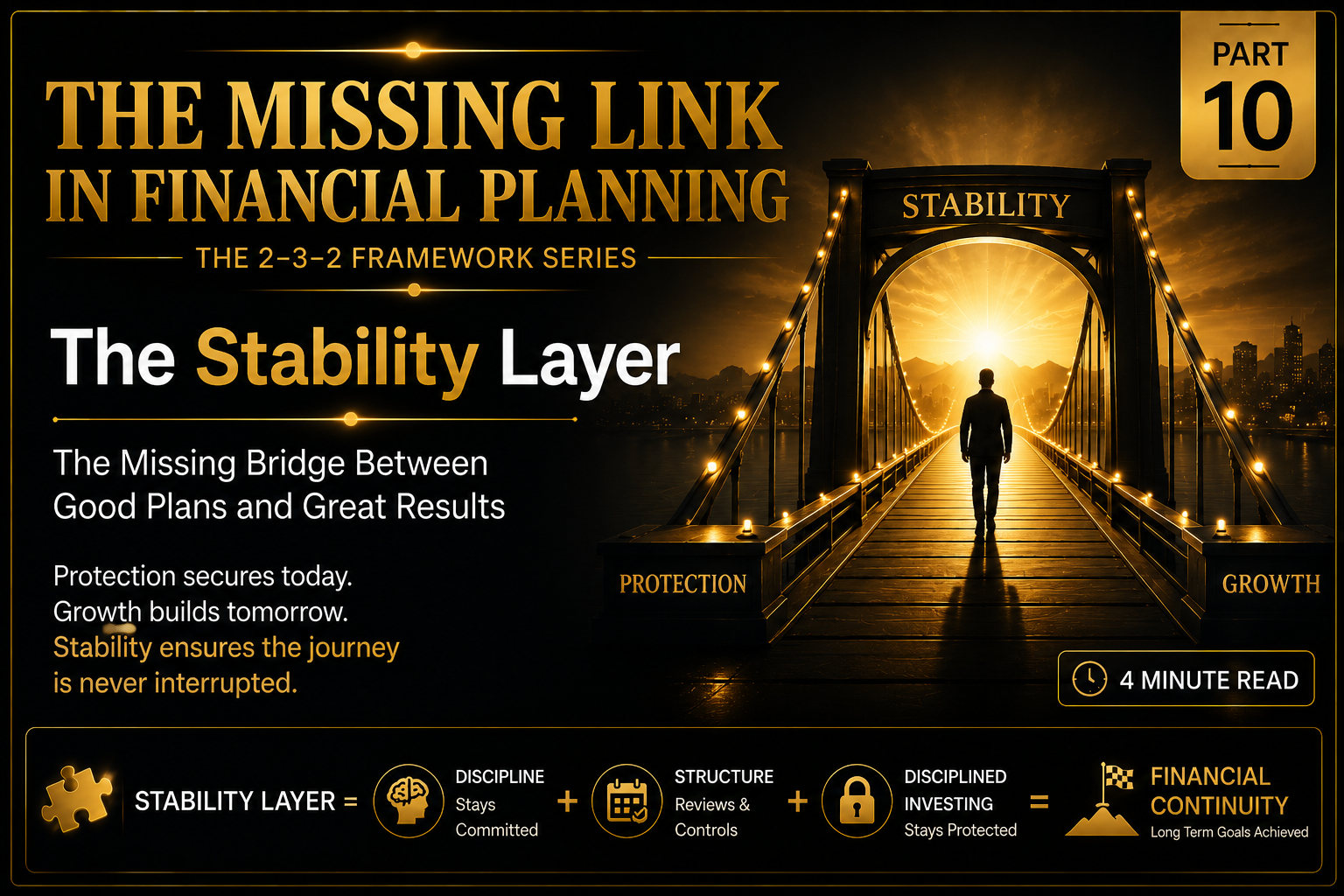

2. Three Layers

- Growth Layer: Designed to build long-term wealth

- Stability Layer: Designed to manage behaviour and reduce emotional reactions

- Protection Layer: Designed to secure the present through risk coverage

3. Discipline Profiling

Understanding investor behaviour and aligning the structure accordingly, ensuring continuity and commitment.

In this framework, the stability layer plays a crucial role. It is where behaviour is accounted for and managed through structure.

The Way Forward

Behavioural finance has helped us understand how investors think and act. However, understanding behaviour alone is not enough.

What is required is a structure that accommodates behaviour and guides it.

If financial planning has to succeed in the real world, it must move beyond return projections and product selection.

It must begin with understanding how people actually behave with money—and then design systems that support discipline.

Because in the end, wealth is not created by the best-performing portfolio.

It is created by the portfolio that investors can stay committed to.

In my next Blog I will talk about why Stability Layer is the Missing Link in Traditional Financial Planning.

Link to Next Blog Part 2 :