The Missing Link in Financial Planning Part 6

June 24, 2026

Understanding the Present Gap

In the earlier parts of this series, I explored why many financial plans fail despite good products and good returns, and how investor behaviour often impacts long-term financial outcomes more than investment performance itself.

In Part 1, I introduced the role of discipline and continuity in making long-term compounding work.

In Part 2, I explored the Stability Layer as a missing dimension in traditional financial planning.

In Part 3, I explained the difference between Investment Volatility Risk and Behavioural Discipline Risk.

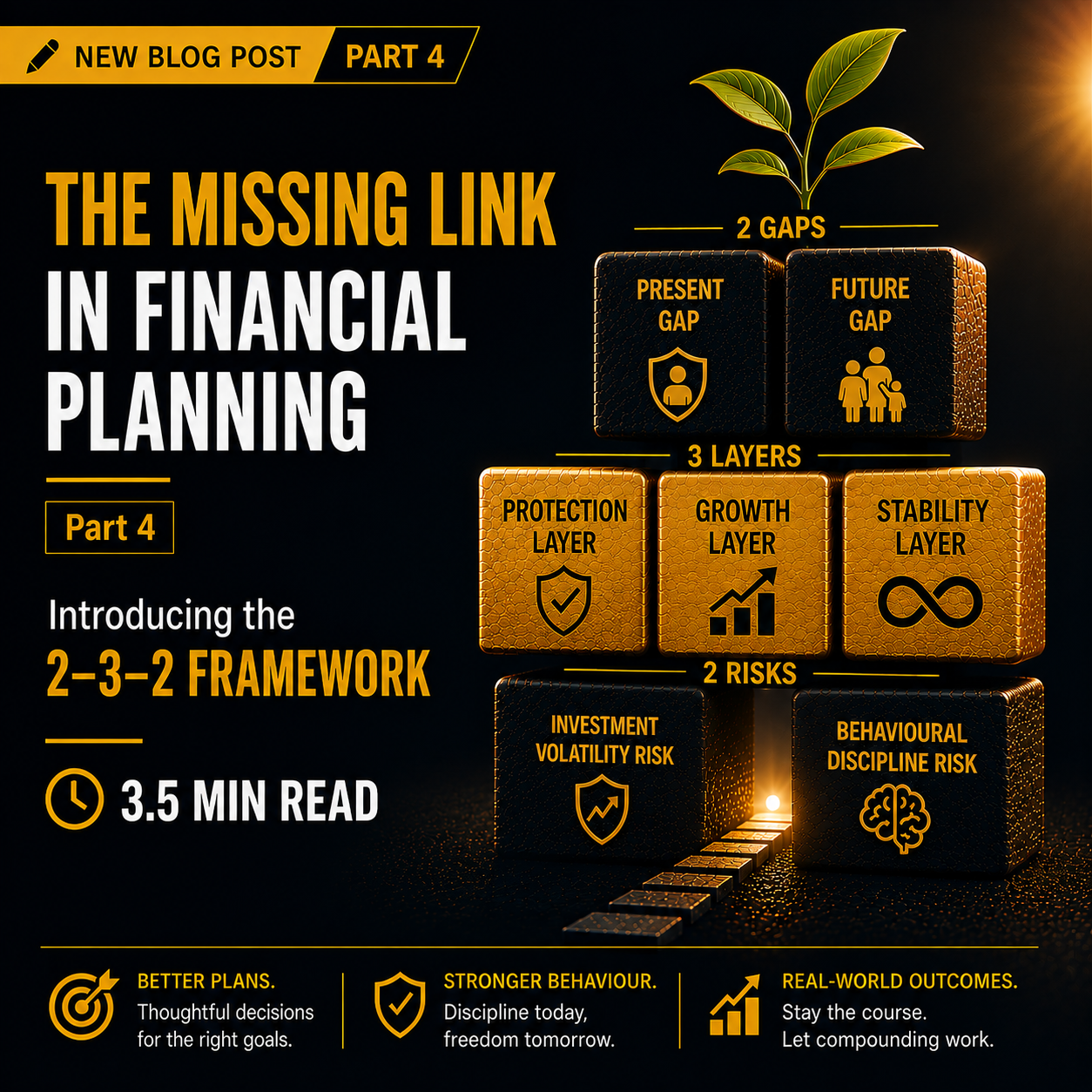

In Part 4, I introduced the 2–3–2 Framework consisting of 2 Gaps, 3 Layers, and 2 Risks.

In Part 5, I introduced the two financial gaps every family must fund — the Present Gap and the Future Gap.

In Part 6, I introduced the two types of goals — Need Goals and Want Goals — and discussed why Need Goals must be funded before Want Goals.

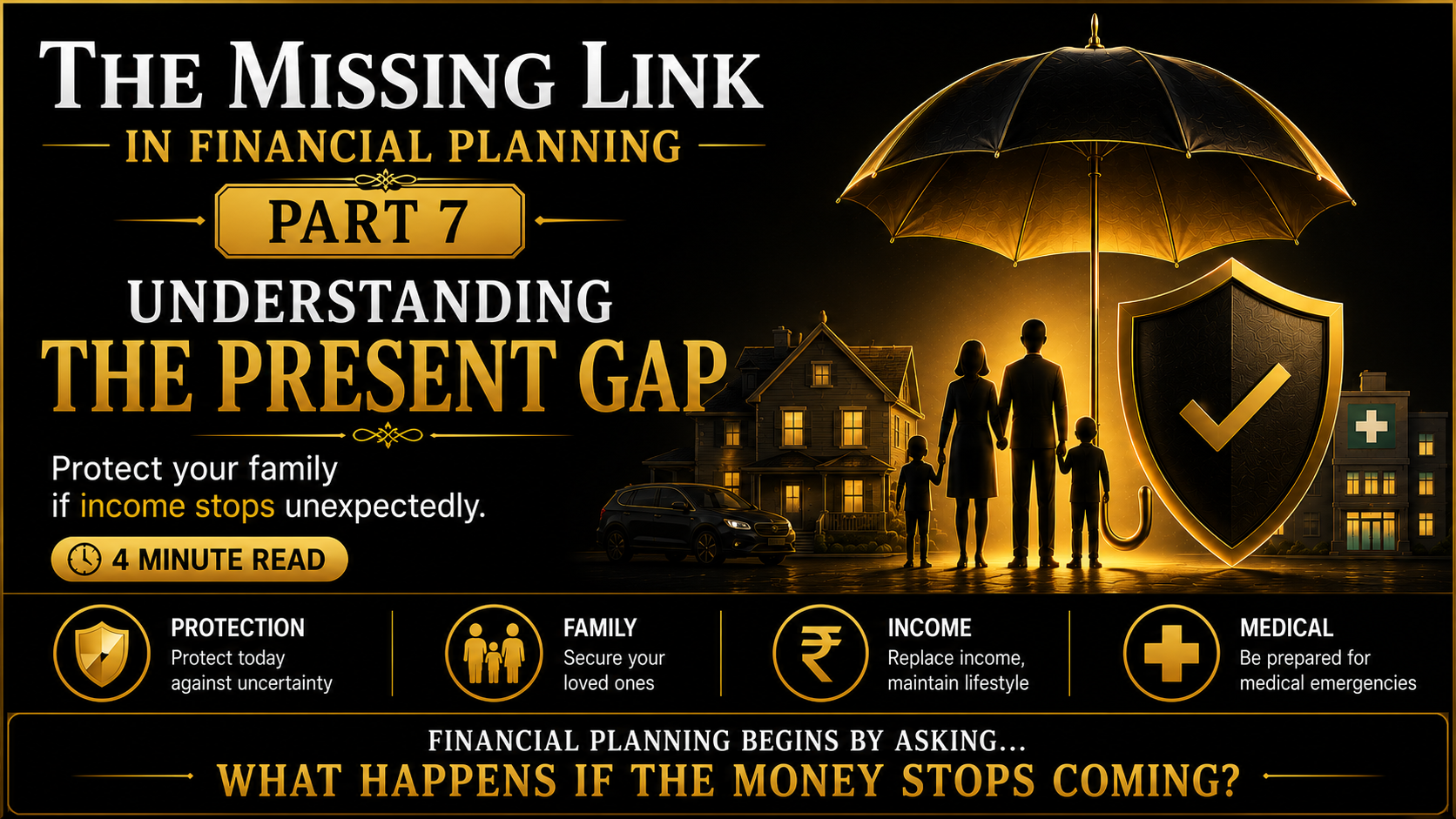

In this article, we focus on the first of the two gaps — the Present Gap.

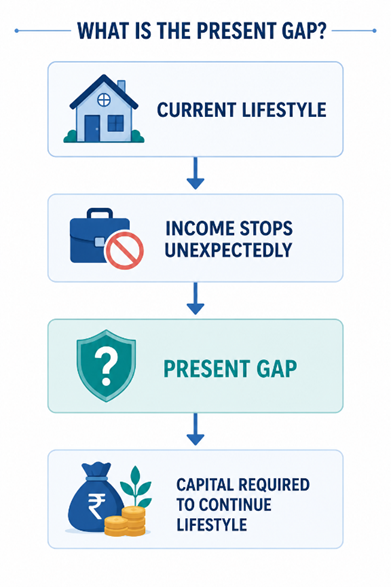

What is the Present Gap?

The Present Gap is the shortage of capital required today to protect a family’s lifestyle if income stops unexpectedly.

Put differently:

If your income stopped tomorrow, would your family be able to continue its current lifestyle without compromise?

The Present Gap arises because of events such as:

• Death

• Disability

• Temporary loss of income

• Medical emergencies

This is not a future problem.

This is a today problem.

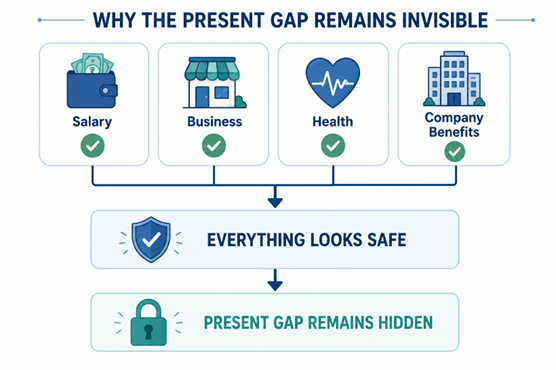

Why Most Families Misunderstand It

Over four decades of working with more than 2,000 families, I have found that most people underestimate the Present Gap because they believe serious financial disruptions happen only to others.

Most people assume:

• Salary will continue

• Business income will continue

• Company benefits will continue

• Health will continue

The Present Gap remains invisible because life appears normal.

Salary arrives every month. Business income continues. Company benefits remain available.

The Present Gap calculation acts like a mirror. It forces families to see today what they would otherwise discover only after an unfortunate event.

Until this calculation is done, many families feel financially comfortable. The moment they calculate their Present Gap, they often discover a significant deficiency in the financial provision required to maintain their lifestyle.

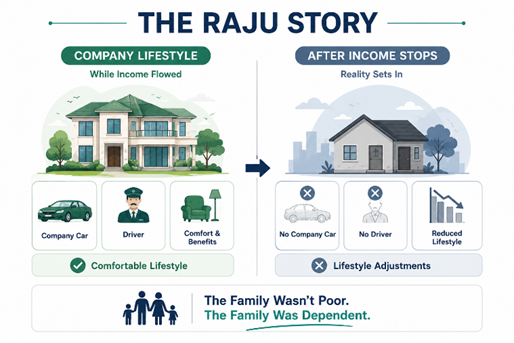

The Raju Story

The story of Raju is a powerful example.

Raju was a senior executive enjoying an excellent lifestyle. The company provided a bungalow, a car, a driver and several benefits. Like many families, they assumed this lifestyle would continue indefinitely.

Unfortunately, Raju passed away unexpectedly.

Within a short period, the bungalow had to be vacated, the company car and driver were withdrawn, and the family had to make painful adjustments to their lifestyle.

They had to move to a smaller home. Expenses had to be reduced. Future plans had to be reconsidered.

Had the family seriously calculated the impact of an unexpected death, they would have realised how dependent their lifestyle was on company-provided benefits.

The key lesson is simple:

The family wasn’t poor. The family was dependent.

Components of the Present Gap

Income Replacement

Can the family continue its lifestyle if the primary earner dies or becomes disabled?

Loan Protection

Can all outstanding loans be repaid without burdening the family?

Medical Emergencies

Can hospital expenses be met without disrupting long-term investments?

Emergency Reserve

Can the family survive six to twelve months without income?

Lifestyle Continuity

Can the family maintain its current standard of living after an adverse event?

Many families mistakenly believe that insurance alone solves the Present Gap.

Insurance is only one part of the solution.

Existing liquid assets, emergency reserves, loan obligations and lifestyle requirements must all be considered before the true Present Gap can be calculated.

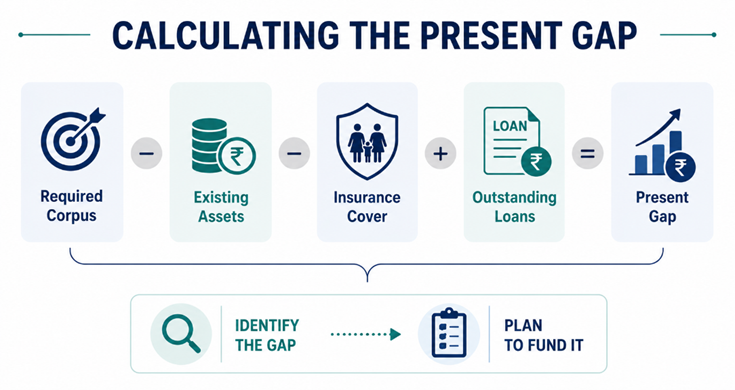

A Simple Illustration of the Present Gap

The Present Gap can be calculated using three simple steps:

Step 1: Calculate the Required Present Corpus

How much capital would be needed to maintain the family’s lifestyle if income stopped?

Step 2: From Required Present Corpus

subtract:

• Existing liquid assets

• Existing insurance cover

Then Add:

• Outstanding loans

To get the Present Gap

Let us take a simple example.

A family spending ₹10 lakh per year may require a corpus of over ₹3 crore to maintain the same lifestyle if income stops.

Most families are surprised when they see this number because they have never viewed their lifestyle as a capital requirement.

Family Expenses: ₹10 lakh per year

Required Corpus: ₹3.33 crore

Liquid Assets = ₹25 lakh

Insurance Cover = ₹1 crore

Outstanding Loan = ₹55 lakh

Present Gap:

₹3.33 crore – ₹25 lakh – ₹1 Crore + ₹55 lakh = ₹2.63 crore

This ₹2.63 crore represents the deficiency in financial provision required to maintain the family’s current lifestyle.

Why This Matters

Most families spend years planning for events that may occur twenty years from now, yet spend very little time preparing for events that could happen tomorrow morning.

The Present Gap is often ignored not because it is unimportant, but because people underestimate low-probability risks.

Unfortunately, when such events occur, the financial consequences can be immediate and severe.

Connection to Stability

The Present Gap forms the foundation of the entire 2–3–2 Framework.

If the Present Gap is ignored, the Protection Layer remains weak.

Without protection, the Growth Layer struggles, and the Stability Layer loses relevance.

Financial continuity begins with securing today’s risks before planning for tomorrow’s goals.

Financial planning begins not by asking how much money you want to make, but by asking:

Present Gap Important question to ask – What happens if the money stops coming?

In the next article, we will explore the second gap in the framework — the Future Gap — and why it is equally critical for long-term financial continuity.