Why Financial Planning Fails Despite Good Returns Part 1

May 19, 2026

The Missing Link in Financial Planning – Part 3

June 3, 2026

Why the Stability Layer may be the missing dimension in long-term financial success.

In my previous article, I introduced the idea that discipline and behaviour play a critical role in making long-term compounding work.

Over four decades of working with more than 2,000 families in financial planning, I repeatedly observed something disturbing — many clients with carefully designed financial plans still failed to achieve their long-term goals.

This forced me to ask an important question:

Why do well-designed financial plans still fail in real life?

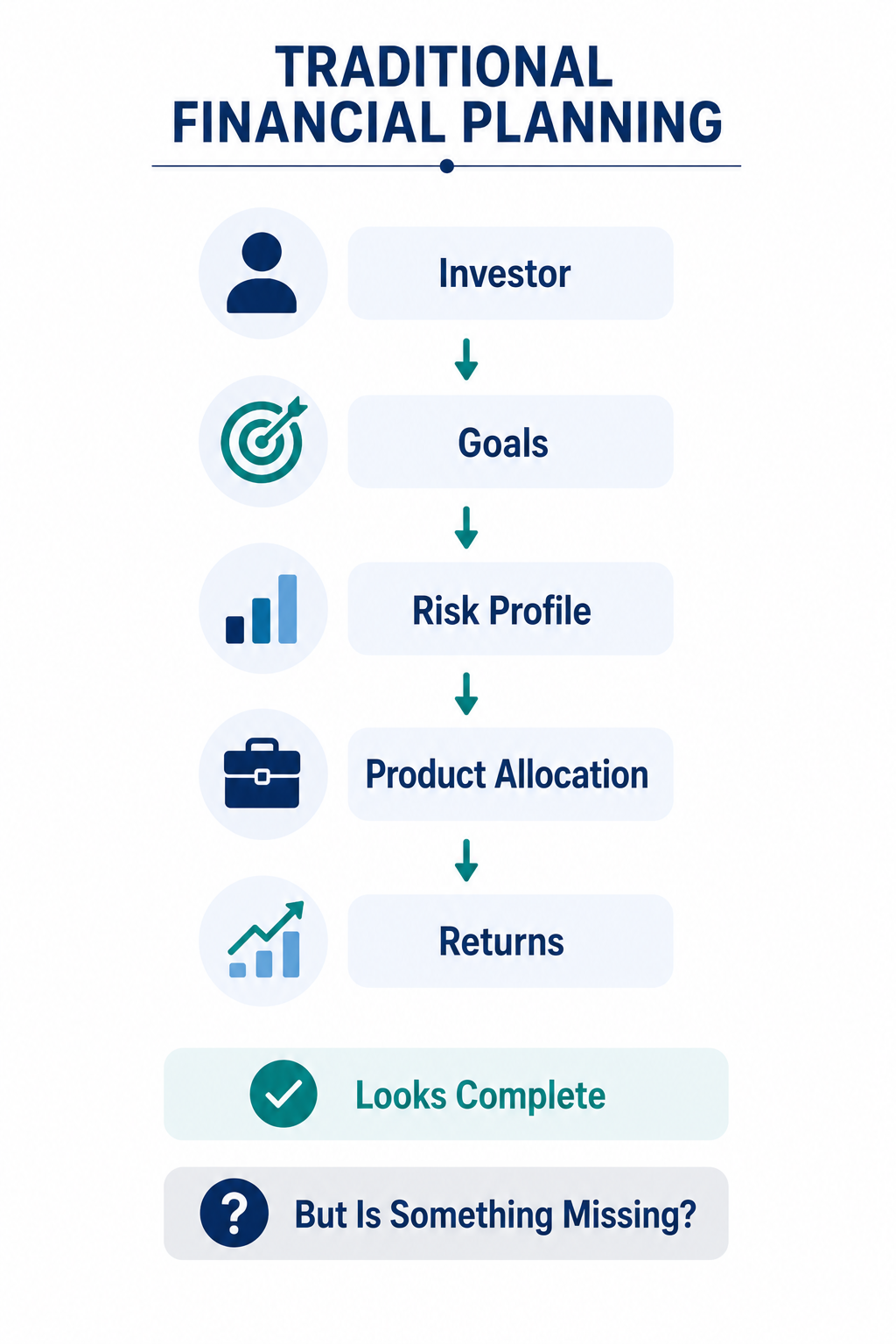

Traditional financial planning already addresses several important dimensions:

- age of the investor

- tenure of goals

- risk appetite

- product allocation

- growth through equity

- protection through insurance

Investors are categorized as aggressive, moderate, or conservative based on their ability to handle volatility and uncertainty.

The framework appears logical and well-structured.

Yet over the years, I found that many investors still fell short when financial responsibilities eventually arrived. Despite years of planning, the required corpus was often missing.

This created what I call:

Long-Term Financial Discontinuity.

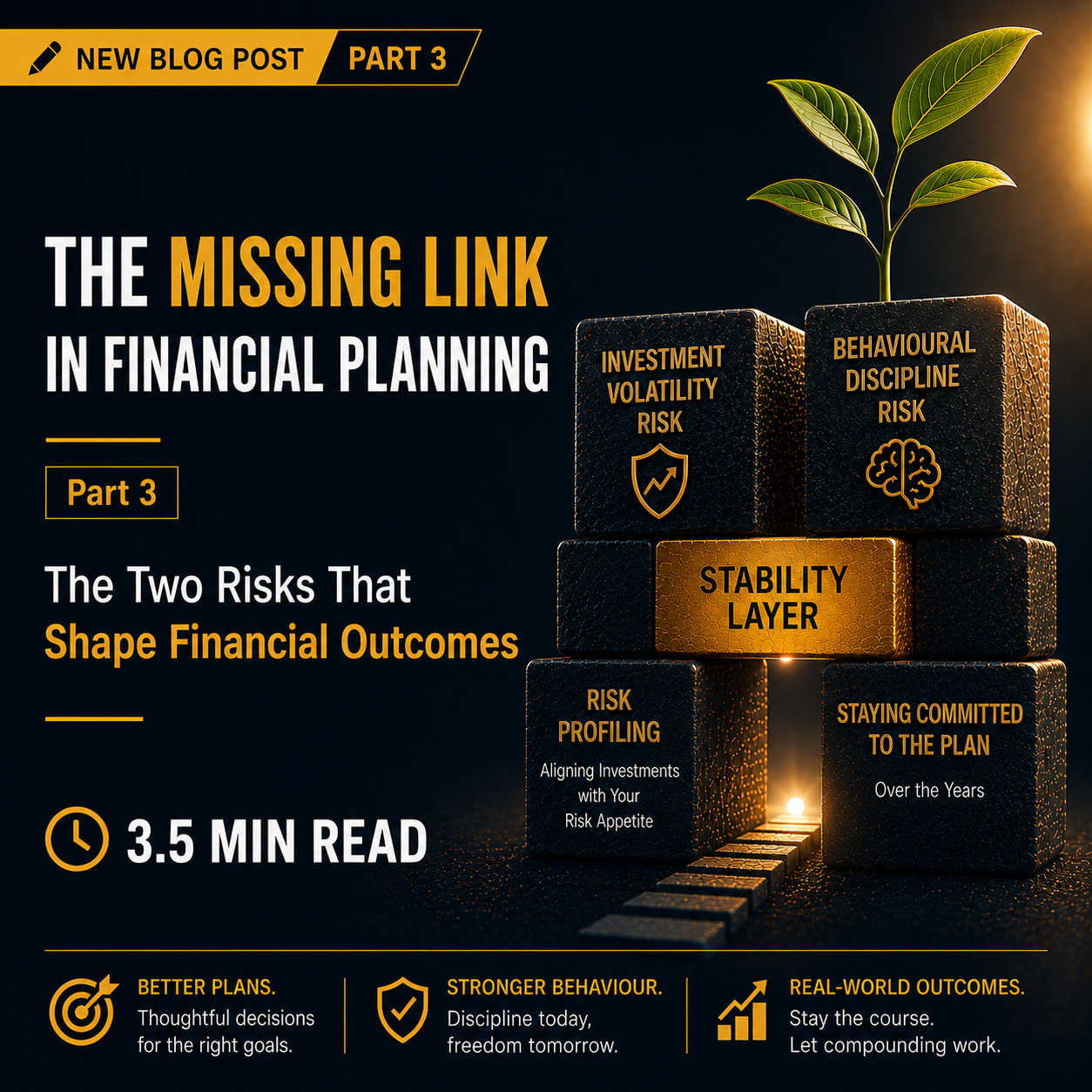

As I explored this problem more deeply, I realized that while behavioural finance explains emotional investor behaviour, there was very little discussion around creating practical structures that help investors sustain discipline over long periods.

Financial outcomes are often shaped more by investor discipline than by the rate of return achieved.

Some disruptions are already addressed through traditional risk profiling — such as fear during market crashes or reactions to volatility.

However, many disruptions are emotional and lifestyle-driven.

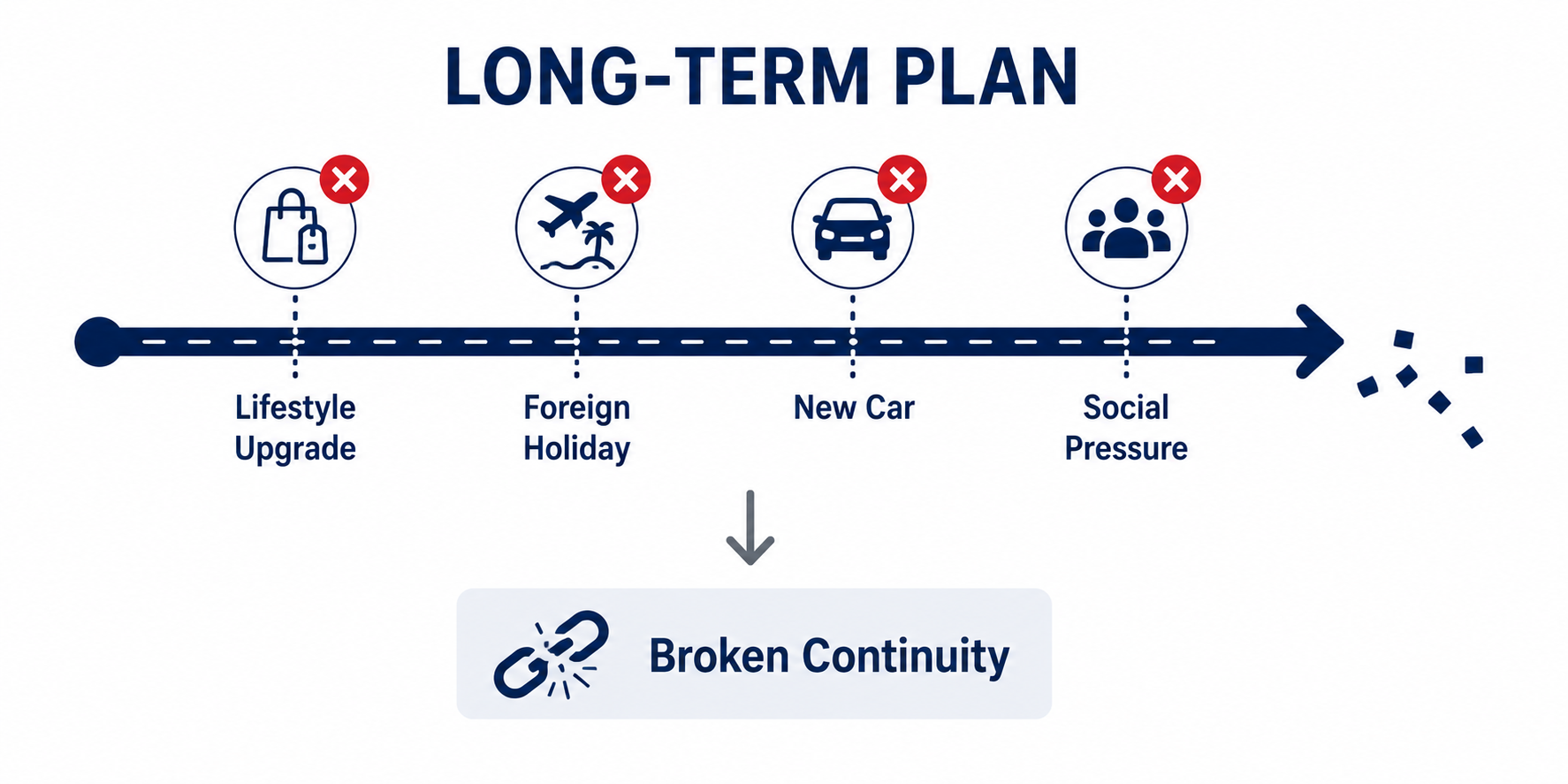

I saw investors interrupt long-term plans because of:

- unplanned purchases

- lifestyle upgrades

- holidays

- social comparison

- short-term temptations

Most investors do not break plans because they lack financial knowledge.

They break them because long-term goals feel distant while immediate temptations feel emotionally stronger.

One small but revealing example was my own PPF account. Like many investors, I had allowed continuity to break over time. I realized that this pattern was not an exception — it was extremely common.

I learned this lesson personally nearly a decade ago when I realized that despite careful planning, I too had missed several of my own long-term investment targets.

The returns on my portfolio were reasonably good — yet the final outcomes still fell short.

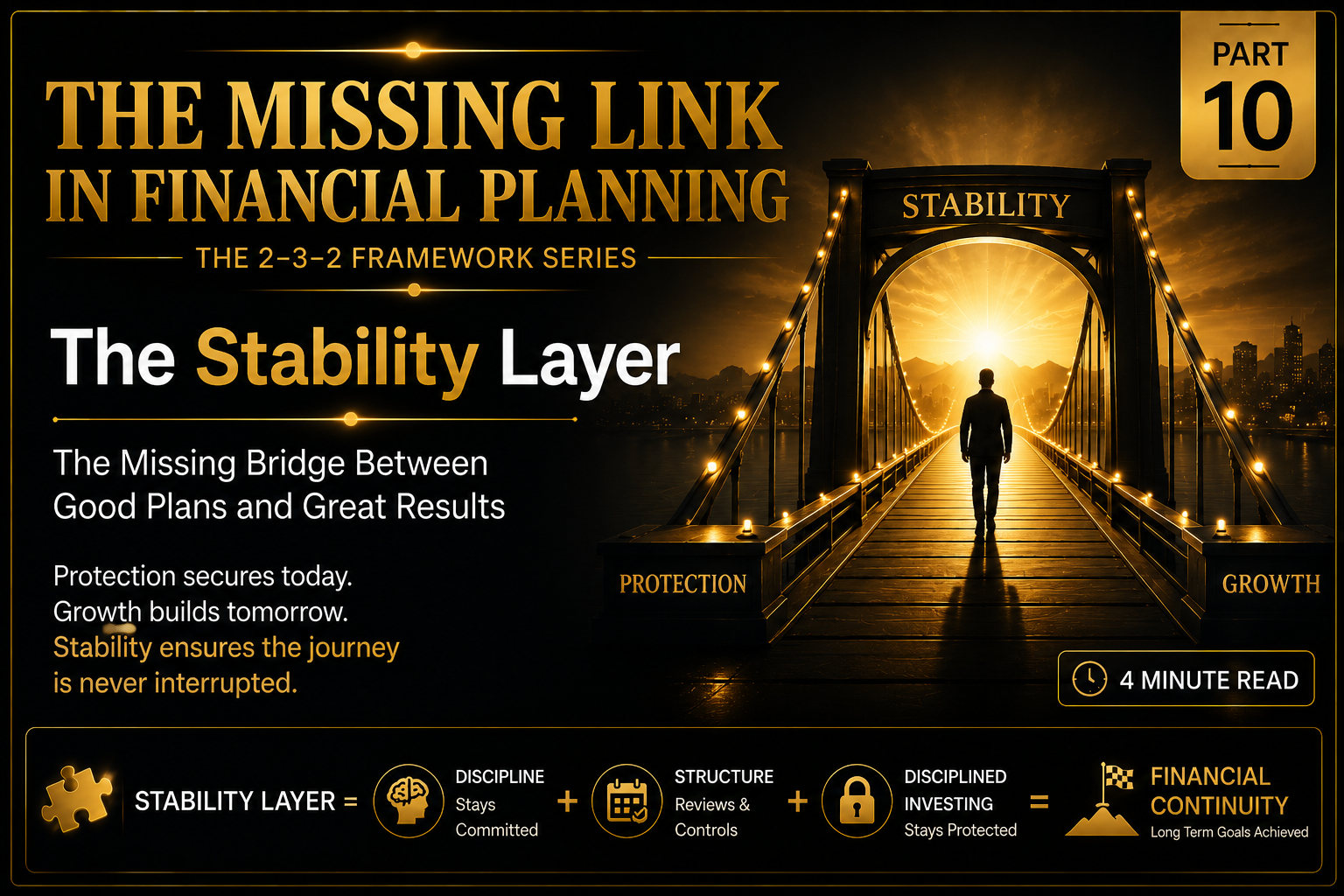

As I reviewed decades of investor behaviour along with my own financial journey, I slowly realized that between Growth and Protection, there was a missing layer:

Stability.

Many fund managers themselves acknowledge that while products may deliver strong long-term returns, investors often fail to experience those outcomes because they do not remain invested long enough.

This raises an important question:

Can a financial plan truly succeed if the investor emotionally cannot sustain the journey long enough for compounding to work?

This realization led me towards what I now call:

The Stability Layer.

The Stability Layer is designed to create behavioural continuity. Its role is to help investors remain committed to their financial journey long enough for compounding to work in their favour.

Behavioural finance has identified several emotional and cognitive biases. However, in my experience, behavioural continuity itself has not been sufficiently addressed structurally within financial planning.

Financial planning is not only about selecting the right products.

It is also about creating structures that help investors remain committed to the journey long enough for compounding to work.

This is where the Stability Layer becomes critical.

In the next article, I will explore how behavioural discipline risk differs from traditional investment risk — and why both need to be addressed separately in financial planning.

Link to Previous PART 1 :https://laazarusdias.in/2026/05/19/why-financial-planning-fails-despite-good-returns/(opens in a new tab)

Link to Next Blog PART 3 :